A strong wealth management report dashboard helps advisors, branch managers, and firm leadership answer one question fast: where are we growing, where are we leaking value, and what action should we take next? In practice, most firms struggle with fragmented CRM records, inconsistent AUM definitions, delayed custodian files, and dashboards overloaded with charts but short on decision support. The business value of getting this right is immediate: better client reviews, cleaner revenue visibility, earlier attrition detection, and faster book-of-business decisions.

Click To Try The Dashboard

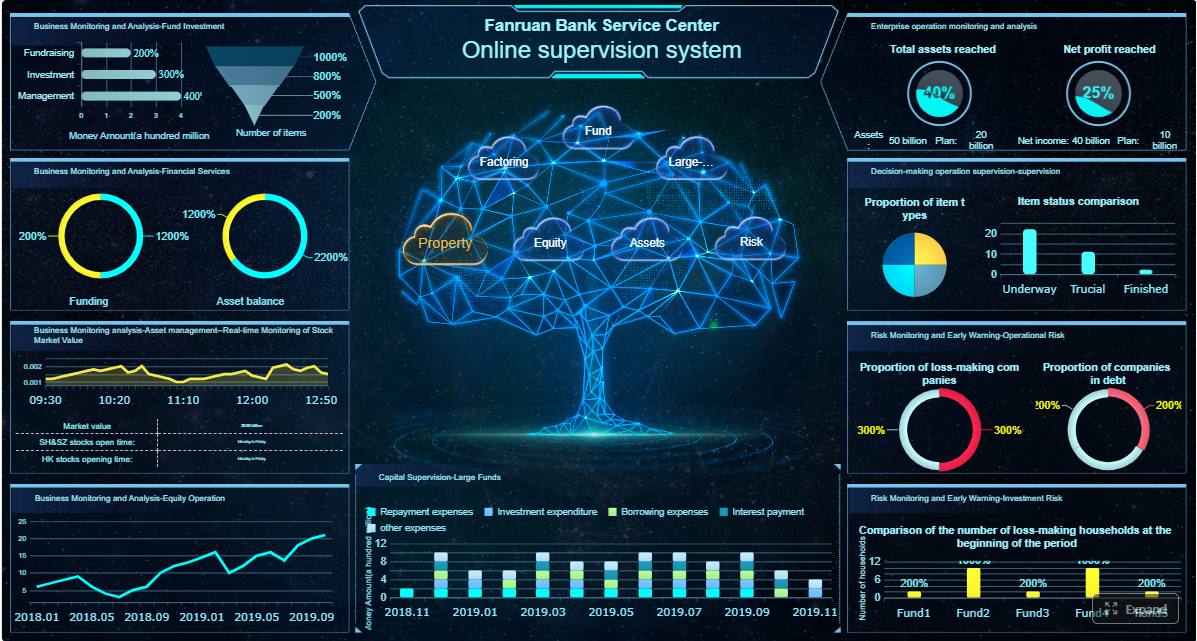

All reports in this article are built with FineReport

What a wealth management report dashboard should achieve

A wealth management dashboard is not just a reporting layer. It is an operating tool for client coverage, growth management, and leadership oversight. Different users need different views, but the dashboard should align them around the same core metrics and definitions.

For advisors and relationship managers, the dashboard should make client review preparation easier. They need to see household assets, recent cash flows, portfolio changes, meeting history, service issues, and revenue contribution in one place. For branch leaders, the focus shifts to team productivity, advisor-level growth, and client retention risk. For firm leadership, the dashboard should summarize strategic performance across offices, channels, and client tiers.

The dashboard should support decisions such as:

Which clients need outreach before the next review cycle

Which advisors are growing net new assets fastest

Which books are profitable but vulnerable to attrition

Whether revenue is on pace against plan

Which service bottlenecks are reducing client satisfaction

Where product mix or portfolio concentration may require attention

Operational monitoring, performance reporting, and strategic planning views

The most effective wealth management report designs separate usage into three views:

Operational monitoring: Daily or near-real-time visibility into flows, service tickets, pending reviews, and exceptions

Performance reporting: Monthly management reporting on AUM, revenue, retention, margins, and advisor productivity

Strategic planning: Quarterly and annual views for growth strategy, segmentation, market opportunity, and resource allocation

This separation matters. A daily dashboard built for operations should not look like a quarterly board pack. Mixing both usually creates clutter and weakens adoption.

Core KPIs to include in a wealth management report

A dashboard only works when it is anchored in a disciplined KPI set. Too few metrics and leaders miss important signals. Too many and no one acts. For most firms, the right answer is a compact first-screen summary with deep drill-downs.

Key Metrics (KPIs)

Assets Under Management (AUM): Total managed client assets at a point in time; the core scale metric for the business

Net New Assets (NNA): New money won minus assets lost; the clearest signal of organic growth

Gross Inflows: New contributions, transfers in, and additional invested assets

Gross Outflows: Withdrawals, transfers out, and closed-account asset exits

Household Growth: Increase in the number of client households over time

Client Retention Rate: Percentage of clients or households retained in a period

Revenue per Household: Average revenue generated from each client household

Recurring Revenue: Ongoing fee-based income generated from advisory relationships

Fee-Based Revenue Mix: Share of total revenue coming from recurring fee arrangements versus transactional revenue

Client-Level Profitability: Revenue minus servicing and support costs at the client or segment level

Share of Wallet: Estimated percentage of the client’s total investable assets held with your firm

Meeting Cadence: Frequency of advisor-client reviews and touchpoints

Service Response Time: Time taken to resolve client requests or operational issues

Advisor Productivity: AUM, revenue, or NNA per advisor or relationship manager

Margin Trend: Profitability trend after operating and servicing costs

Cross-Sell Penetration: Number or percentage of clients using multiple products or advice services

Attrition Risk Flag: Early warning indicator based on withdrawals, inactivity, complaint patterns, or reduced engagement

Client and asset growth metrics

The growth layer of a wealth management report should answer whether the firm is expanding client relationships in a healthy, sustainable way. AUM remains foundational, but it is incomplete on its own because market appreciation can mask weak organic growth.

The most useful growth metrics include:

AUM by advisor, office, region, and client segment

Net new assets by month, quarter, and year

Household growth by advisor and branch

Inflows versus outflows by client tier

New account openings and closures

Portfolio-type growth across discretionary, advisory, retirement, and alternative allocations

A consultant’s recommendation: always separate market-driven AUM growth from organic asset growth. Leadership should be able to see whether performance is coming from new client wins, wallet expansion, or simply favorable market conditions.

Segmentation is equally important. The dashboard should allow users to compare performance by:

Advisor

Office or branch

Client tier

Household type

Portfolio type

Region

Channel or business line

Revenue and profitability indicators

Growth without revenue quality can create misleading optimism. A strong wealth management report must show how asset growth converts into sustainable profitability.

Core revenue and profitability indicators should include recurring advisory fees, planning revenue, transactional revenue where relevant, and margin contribution by segment. Leadership should also be able to compare actuals against targets, prior periods, and expected benchmark ranges.

Critical indicators include:

Recurring revenue trend

Fee-based revenue as a percentage of total revenue

Product mix by revenue contribution

Revenue by advisor and office

Revenue per client or household

Margin trend by segment

Client-level profitability

Target versus actual attainment

A practical point: client-level profitability often reveals service model issues. Some households produce strong gross revenue but consume disproportionate service effort. Your dashboard should highlight these cases so leaders can redesign coverage models, pricing, or service tiers.

Client engagement and retention signals

In wealth management, attrition rarely arrives without warning. Signals usually appear first in behavior: fewer meetings, declining wallet share, unusual withdrawals, slow follow-up, or rising service complaints. That is why engagement metrics deserve equal prominence alongside AUM and revenue.

Useful retention and engagement metrics include:

Retention rate by client tier and advisor

Share of wallet estimate

Review meeting cadence

Digital engagement or portal usage, where available

The dashboard should also surface early warning signs for advisors, such as:

Large outflows after prolonged inactivity

Missed annual review milestones

Service tickets open beyond SLA

Sudden drop in communication frequency

Revenue decline from historically stable households

This is where a good wealth management report becomes operationally valuable. It moves teams from passive reporting to proactive intervention.

Data sources and inputs that power the dashboard

A dashboard is only as reliable as the systems feeding it. In wealth management, the complexity comes from multiple platforms that were not built with shared identifiers or unified metric definitions.

Internal systems and firm data

Most firms need to combine data from several internal sources:

Service or case management tools: Requests, complaints, response times, and issue categories

The common failure point is not extraction. It is ownership. Every metric in the wealth management report should have a business owner, a technical owner, a refresh schedule, and a clear calculation rule.

Set explicit standards for:

Data refresh timing

Source system priority

Exception handling

Missing value logic

Reconciliation thresholds

Metric sign-off responsibility

External research and market intelligence

External data does not usually drive operational reporting, but it strengthens strategic interpretation. Firms can use reputable industry studies and market intelligence to contextualize trends in client behavior, advisor productivity, fee pressure, product adoption, and broader wealth market shifts.

Use external inputs to enrich:

Benchmark ranges for growth and retention

Peer context for revenue mix or fee-based adoption

Investor behavior trends

Market environment commentary for executive reviews

Strategic planning around segmentation, personalization, and portfolio demand shifts

The key is restraint. Do not clutter the main dashboard with too much outside data. Instead, layer benchmark context into executive and quarterly views where it improves interpretation.

Data modeling and governance basics

This is the part many firms underestimate. Without clean data modeling, even a visually polished dashboard will fail in executive review.

At minimum, standardize these entities across systems:

Client ID

Household ID

Advisor ID

Account ID

Office or branch ID

Product or portfolio category

Revenue category

Then create a metric dictionary that defines exactly how the dashboard calculates AUM, NNA, recurring revenue, retention, profitability, and other core measures.

This governance layer is what makes the wealth management report trustworthy enough for both advisor action and executive decision-making.

How to design the reporting workflow

A dashboard project fails when teams focus only on the visual layer and ignore reporting operations. The workflow must be designed end to end, from extraction to publishing, with clear roles and controls.

From data collection to dashboard delivery

A mature reporting workflow typically follows this sequence:

Extract data from CRM, custodians, accounting, billing, and compliance systems

Validate completeness, file freshness, and structural integrity

Transform data into standardized entities and calculated metrics

Reconcile critical values such as AUM, revenue, and flows against source totals

Review dashboard outputs with data owners or business analysts

Publish approved views to the right user groups

Distribute reports through scheduled refreshes, subscriptions, or portal access

Define roles clearly:

Operations or data engineering prepares feeds

Finance validates revenue-related outputs

Wealth leadership or reporting managers approve KPI presentation

Advisors, managers, and executives consume role-based views

This role clarity reduces disputes about numbers and speeds up reporting cycles.

Reporting cadence and audience views

Not every user needs the same update frequency. Matching cadence to decision needs improves usability and performance.

Recommended structure:

Daily monitoring: Flows, service issues, review schedules, exceptions, and key client activity

If the dashboard is used in regulated or client-facing contexts, governance should be designed in from day one, not added later.

Best practices for building a dashboard advisors will actually use

Adoption is the real test. A dashboard that looks sophisticated but does not help advisors act will be ignored within weeks.

Keep the interface clear and actionable

The first screen should answer the most important business questions at a glance. Put high-value KPIs front and center, then allow drill-down into client, advisor, office, or segment details.

Use these design principles:

Lead with decision-ready KPIs

Put AUM, NNA, revenue, retention, and key alerts on the first screen.

Reduce visual clutter

Do not overload the page with redundant charts, decorative graphics, or low-value metrics.

Use meaningful filters

Let users slice by advisor, office, household tier, product type, and date range.

Support drill-down paths

Users should move from executive summary to advisor view to client-level detail without leaving the reporting environment.

Show comparisons clearly

Include prior period, target, and benchmark comparisons where they support action.

A dashboard becomes useful when it prompts follow-up action, not just observation.

Best practices from implementation projects:

Attach thresholds to metrics

Define green, amber, and red conditions for retention risk, outflows, stale reviews, and service delays.

Build alerts for priority events

Trigger notifications for large withdrawals, missed client reviews, or deteriorating wallet share.

Align outputs with advisor workflows

Make sure dashboard insights can be used directly in client review prep, growth planning, and service management.

Add follow-up logic

For example, if a household has declining assets and no meeting in 180 days, create a follow-up task for the advisor team.

Review usage data

Track which views users open, which filters they apply, and where they drop off. This reveals what is useful and what should be simplified.

These steps separate a reporting artifact from a working management tool.

Focus on AUM, NNA, recurring revenue, retention, and service alerts

Launch role-based views for a small pilot group

Phase 2: Improve segmentation and drill-down

Add advisor, office, household tier, and portfolio segmentation

Introduce target comparisons and period-over-period views

Refine filters and navigation based on user feedback

Phase 3: Add intelligence and automation

Introduce attrition flags, thresholds, and alerts

Automate distribution and scheduled refreshes

Add executive summary pages for monthly and quarterly reviews

Phase 4: Strengthen governance

Finalize the metric dictionary

Formalize reconciliation and approval workflows

Expand audit trails, role permissions, and compliance controls

This phased model lowers risk, speeds adoption, and prevents the team from getting stuck in months of design without business impact.

Build the dashboard faster with FineReport

Building this manually is complex; use FineReport to utilize ready-made templates and automate this entire workflow.

For enterprise wealth management teams, the challenge is rarely just visualization. It is integrating multiple systems, standardizing KPI definitions, supporting role-based access, and delivering reliable reports on schedule. FineReport helps solve that by giving firms a practical way to build dashboards, automate refreshes, manage permissions, and publish different views for advisors, managers, and executives without relying on fragile spreadsheet chains.

FineReport is especially well suited when you need to:

Consolidate CRM, custodian, billing, and portfolio data

Strengthen governance with controlled publishing and access

Scale from pilot dashboards to enterprise-wide reporting

If your current reporting process depends on manual exports, spreadsheet merging, and repeated reconciliation, the cost is not just time. It is slower decisions, weaker advisor adoption, and lower trust in the numbers. FineReport gives you a faster path to a dashboard that is operationally useful and executive-ready.

Start with a compact summary of core KPIs such as AUM, net new assets, inflows, outflows, client retention, revenue, and advisor productivity. Then add drill-downs by advisor, branch, segment, and household so users can move from signal to action quickly.

Net new assets should separate organic client-driven flows from market performance so growth is not overstated. A clear calculation usually combines new money in, money out, transfers, and closed-account asset movement for the selected period.

Most firms need data from CRM systems, portfolio accounting platforms, custodian files, revenue or billing systems, and service or ticketing tools. Accuracy depends on reconciling definitions and refresh timing across these sources before metrics reach the dashboard.

It depends on the use case. Operational views may need daily or near-real-time updates, while performance reporting is often monthly and strategic planning is usually quarterly or annual.

Common problems include inconsistent AUM definitions, mixing market gains with real asset growth, fragmented client records, and dashboards with too many charts but too little decision support. The best reports keep metric definitions consistent and organize views by operational, management, and strategic needs.

Product Trial

FineReport

Pixel-perfect reports · Interactive dashboards · Easy data entry · Digital twins