Record to report process outsourcing helps finance leaders reduce close delays, improve control execution, and lower the cost of running routine accounting operations. For CFOs, controllers, shared services leaders, and finance operations managers, the pain points are familiar: month-end closes that drag on, reconciliations that pile up, inconsistent review practices across entities, and high-value finance staff stuck doing repetitive work instead of analysis. A well-designed outsourcing model addresses these issues by standardizing close activities, clarifying accountability, and bringing tighter operational discipline to the record-to-report cycle.

Click To Try The Dashboard

All reports in this article are built with FineReport

Record to report process outsourcing refers to outsourcing all or part of the finance activities that turn raw accounting transactions into finalized financial statements and management reports. In plain language, it covers the path from recording transactions, posting journals, reconciling balances, and managing the close to preparing reports for leadership, auditors, and regulators.

This is broader than simply outsourcing bookkeeping support. The record-to-report cycle usually includes a structured sequence of accounting and reporting activities that must happen accurately and on time every period.

Core elements of the record-to-report cycle

Transaction capture: Recording financial activity from source systems into the ERP or accounting platform.

Journal entry processing: Preparing, reviewing, posting, and documenting recurring and non-recurring journals.

Account reconciliations: Matching subledgers and supporting schedules to the general ledger and resolving discrepancies.

Close management: Coordinating calendars, checklists, dependencies, and period-end tasks across teams and entities.

Intercompany accounting: Managing intercompany balances, eliminations, and settlement issues.

Consolidation support: Rolling up financial data across business units, legal entities, or regions.

Financial reporting: Producing trial balances, management packs, statutory reports, and close summaries.

Control documentation: Retaining evidence, documenting approvals, and supporting internal or external audits.

What is commonly outsourced vs retained in-house

In many enterprises, outsourced teams handle repeatable, rules-based activities, while internal finance retains ownership of judgment-heavy, business-critical decisions.

Commonly outsourced activities:

Balance sheet reconciliations

Journal preparation and posting support

Close calendar coordination

Variance reporting and routine management reports

Intercompany matching and issue follow-up

Fixed asset accounting support

Supporting schedule preparation

Control evidence collection and retention

Commonly retained in-house:

Final financial statement sign-off

Accounting policy interpretation

Material judgments and reserves

Executive reporting to the board

Audit committee communications

High-risk or highly sensitive entries

Strategic finance analysis and planning

How outsourcing differs from staff augmentation or AP/AR support

Record to report process outsourcing is not the same as adding temporary accountants to your team. Staff augmentation fills labor gaps, but your organization still owns process design, training, management, and control consistency. By contrast, outsourcing transfers a defined scope of work with documented responsibilities, service levels, and governance.

It is also different from transactional AP or AR outsourcing. Accounts payable and accounts receivable support focus on invoice processing, collections, and cash application. Record to report sits closer to the finance control tower. It is responsible for period-end integrity, reconciliation discipline, and reporting quality across the broader accounting environment.

The business problems this model is meant to solve

Companies typically adopt record to report process outsourcing when finance operations become too slow, too manual, or too inconsistent to scale.

Common issues include:

Slow month-end and quarter-end close cycles

Fragmented controls across legal entities or business units

Reconciliation backlogs and unresolved exceptions

High dependence on key individuals

Limited visibility into close progress

Rising finance overhead without corresponding efficiency gains

Burnout among internal accounting managers and controllers

Why companies use it to close faster and reduce finance overhead

The main business case for record to report process outsourcing is straightforward: improve close performance while controlling cost. When implemented correctly, it creates a more repeatable operating model and frees internal finance capacity for analysis, planning, and risk management.

Shorter close timelines without sacrificing reporting quality

Closing faster does not come from pushing people harder. It comes from reducing ambiguity. Outsourced record-to-report teams usually bring standardized workflows, documented handoffs, defined cutoff times, and tighter close calendars.

That structure reduces common sources of delay such as:

Missing support for journal entries

Late reconciliations

Unclear ownership of close tasks

Inconsistent cutoff application

Ad hoc review cycles

Rework caused by formatting or data issues

With a disciplined operating cadence, organizations can reduce close days while maintaining reporting quality and audit traceability.

Better use of finance talent and management attention

High-performing finance functions do not want senior accountants spending most of their time clearing routine reconciliations or assembling repetitive reports. Outsourcing allows internal teams to focus on value-added responsibilities such as:

This is often where the real ROI appears. The benefit is not only labor arbitrage. It is redeploying scarce finance talent to work that materially improves decision-making.

More predictable costs and scalable support

Internal finance cost structures are often fixed. Headcount, overtime, training, and management overhead remain in place even when workload fluctuates. Record to report process outsourcing creates more flexibility, especially for businesses with:

Multi-entity close requirements

Seasonal reporting peaks

M&A integration activity

Global operations across time zones

Frequent changes in reporting volume

An outsourced model can scale support during close-intensive periods without forcing permanent internal hiring.

Key Metrics (KPIs) to manage this scenario

For enterprise decision-makers, success should be measured with a tightly defined KPI set.

Days to close: Total business days from period end to final management or statutory reporting.

Reconciliation completion rate: Percentage of assigned reconciliations completed by deadline.

Aged unreconciled items: Value or count of reconciling items unresolved beyond policy thresholds.

Journal turnaround time: Time from journal preparation to approval and posting.

Review timeliness: Percentage of reviews completed within the planned close calendar.

Close task completion rate: Share of scheduled close activities completed on time.

Error rate: Number of reporting or posting errors identified after close.

Rework volume: Tasks or entries requiring correction due to incomplete support or review gaps.

Cost per close cycle: Fully loaded finance operating cost per monthly or quarterly close.

Audit evidence completeness: Percentage of key controls with complete and retrievable support.

7 ways to strengthen controls and cut overhead through outsourcing

The most effective outsourcing arrangements do not just shift work. They redesign the operating model so controls are easier to execute and routine cost is easier to manage.

1. Standardize close activities across entities and periods

Many finance teams struggle because each entity closes differently. Different templates, different naming rules, different deadlines, and different review habits create avoidable variation.

A stronger outsourced model uses:

Common close calendars

Standard task checklists

Shared journal templates

Uniform reconciliation formats

Clear cutoff conventions

Consistent sign-off rules

Standardization reduces missed steps, lowers training burden, and makes performance easier to compare across entities.

2. Improve reconciliations and exception handling

Reconciliations are often where control breakdowns become visible. If balances stay unresolved month after month, close quality deteriorates and audit risk rises.

Best-in-class outsourced teams establish:

Clear preparer and owner assignments

Aging thresholds for open items

Escalation rules for unresolved differences

Root-cause tracking for recurring exceptions

Priority handling for material accounts

This creates discipline around cleanup rather than allowing issues to roll forward indefinitely.

3. Build stronger review and approval workflows

Strong controls depend on documented review, not informal oversight. One of the biggest improvements outsourcing can bring is more consistent workflow design.

That means separating duties between:

Preparer

Reviewer

Approver

Final process owner

Each step should be time-bound and evidenced. This improves accountability while reducing the chance that entries or reconciliations are approved without adequate support.

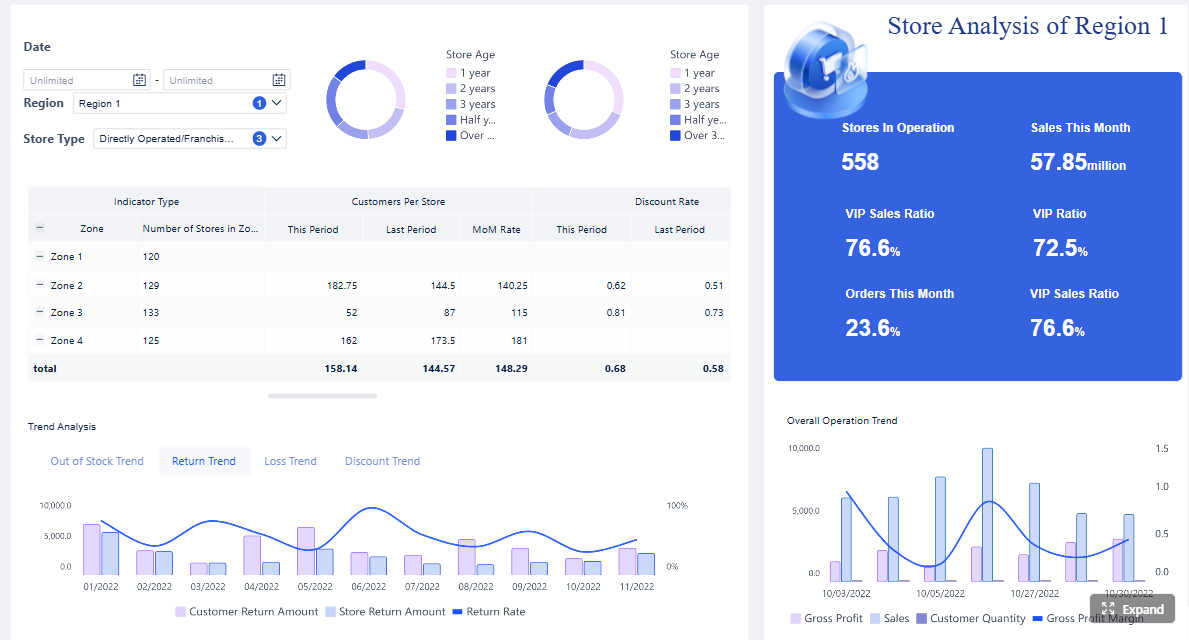

4. Increase visibility with dashboards and close metrics

Finance leaders cannot manage what they cannot see. Dashboards make close operations measurable and help surface bottlenecks before they jeopardize reporting deadlines.

With this visibility, controllers can intervene early instead of discovering issues late in the close cycle.

5. Use automation for journals, matching, and reporting tasks

Manual effort is expensive and inconsistent, especially in high-volume accounting processes. Outsourcing becomes much more effective when paired with workflow and reporting automation.

The goal is not to remove controls. It is to reduce manual touchpoints while preserving a complete audit trail.

6. Tighten policy adherence and documentation standards

Control quality weakens quickly when procedures live in email threads or tribal knowledge. Outsourced record-to-report teams should operate from current and documented standards.

That includes:

Standard operating procedures

Control narratives

Approval matrices

Evidence retention rules

Naming and filing conventions

Review checklists

Good documentation reduces dependence on specific individuals and improves audit readiness.

7. Align service levels to business needs and risk areas

Not every process needs the same speed or level of review. The best outsourcing models apply service levels based on business importance and control risk.

For example:

Material accounts get tighter review deadlines

Statutory reporting tasks receive higher priority than internal low-risk reports

Complex entities get more senior oversight

Peak close windows receive expanded support coverage

This risk-based service design helps companies spend money where it matters most.

Actionable best practices for implementing record to report process outsourcing

If you want outsourcing to improve control and not just move work offshore, execution matters. These are the practices seasoned finance transformation teams prioritize first.

1. Start with a process and control baseline

Before transitioning work, document the current state in detail.

Map every close activity by owner, frequency, dependency, and due date

Identify high-risk accounts, bottlenecks, and recurring exceptions

Separate judgment-based tasks from repeatable execution tasks

Confirm which controls must remain internal

Without this baseline, organizations outsource confusion instead of outsourcing a process.

2. Design ownership down to the task level

Ambiguity destroys close performance. Define responsibility with precision.

Who prepares journals?

Who reviews reconciliations?

Who manages open item escalation?

Who owns entity-level close status?

Who has final approval rights?

Use a RACI model if needed, but make it operational, not theoretical.

3. Build the transition around the close calendar

Do not migrate work in a way that disrupts critical reporting periods.

Transition lower-risk activities first

Pilot with selected entities or account groups

Run parallel close cycles where necessary

Stabilize documentation before expanding scope

The safest transitions are phased and measured.

4. Create a formal governance rhythm

Outsourcing relationships perform best when governance is regular and data-driven.

Weekly operational reviews during transition

Monthly KPI reviews after go-live

Quarterly scope and control assessments

Structured issue logs and remediation tracking

This prevents small execution problems from becoming control failures.

5. Instrument the process with dashboards from day one

If the provider cannot show task status, aging, productivity, and exceptions in near real time, management control will remain weak.

What a well-designed outsourced record-to-report model looks like

The difference between a risky outsourcing arrangement and a high-performing one is usually design discipline. A strong model has clear scope, the right technology foundation, and a control environment that can stand up to audit scrutiny.

Scope, roles, and governance

A mature model clearly defines who owns each step of the cycle. At minimum, responsibilities should be explicit for:

Journal preparation

Journal approval

Reconciliations

Close task management

Consolidation support

Variance reporting

Final reporting approval

Governance should include service review meetings, KPI reporting, escalation channels, and a clear path for handling policy questions or unusual transactions.

Technology and data access

The provider cannot operate effectively without fit-for-purpose systems access and reporting infrastructure. Common requirements include:

ERP or general ledger access with role-based permissions

The design principle is simple: enough access to execute work efficiently, but not so much that control boundaries are blurred.

Control environment and audit readiness

A good outsourced model should strengthen audit readiness, not weaken it. Evidence should be retained consistently, reviews should be visible, and exceptions should be traceable from identification through resolution.

How to evaluate providers and plan a smooth transition

Selecting a provider should be treated as an operating model decision, not a procurement exercise alone. The right partner must demonstrate accounting depth, close discipline, reporting capability, and control maturity.

Questions to ask before selecting a partner

Use provider discussions to test real execution capability.

Ask questions such as:

How do you manage close calendars across multiple entities?

What reconciliation governance practices do you use?

How do you separate preparer and reviewer roles?

How do you handle recurring exceptions and stale balances?

What dashboards do you provide for close visibility?

What is your approach to SOP maintenance and control evidence?

How do you support audit requests during peak periods?

What experience do you have in our industry and reporting environment?

Transition risks to manage early

Most outsourcing failures can be traced back to a few preventable issues.

Watch for:

Unclear process ownership

Undocumented exceptions and workarounds

Poor chart of accounts or master data quality

Inconsistent entity calendars

Incomplete SOPs

Unstable source system feeds

Overreliance on individual employees for process knowledge

Addressing these upfront reduces disruption after go-live.

Metrics to track after go-live

The first 90 to 180 days after transition are critical. Track outcomes closely to ensure the model is delivering both cost and control improvements.

Priority post-go-live metrics include:

Days to close

Reconciliation completion rates

Review timeliness

Open item aging

Journal error rates

On-time reporting delivery

SLA performance

Cost per close cycle

These measures should be reviewed at both the process level and the entity level to expose hidden variance.

Building this manually is complex; use FineReport to automate the workflow

Building this manually is complex; use FineReport to utilize ready-made templates and automate this entire workflow. For companies pursuing record to report process outsourcing, reporting and visibility are often the weakest links. Teams may have the right people and documented processes, but still lack a reliable way to monitor close progress, reconciliation status, approval bottlenecks, and control evidence in one place.

FineReport helps finance teams and outsourcing managers turn fragmented close data into operational dashboards that are easy to act on. Instead of stitching together spreadsheets, email updates, and static reports, teams can build a centralized view of:

Close task progress by entity

Reconciliation completion and aging

Journal workflow turnaround

Reviewer bottlenecks

SLA adherence

Audit support status

This matters because outsourcing success depends on transparency. If leadership cannot see whether controls are being executed on time, cost savings will come with hidden risk. FineReport gives finance operations a scalable reporting layer so managers can identify delays early, enforce accountability, and keep the close moving.

It also reduces dependence on manual reporting preparation. With ready-made templates, automated data integration, and customizable dashboards, finance teams can support an outsourced model without creating another reporting burden internally.

For enterprise teams that want faster closes, stronger controls, and lower finance overhead, FineReport is a practical enabler of the operating model.

It is the outsourcing of finance activities that move data from accounting transactions to finalized financial statements and management reports. This usually includes journals, reconciliations, close coordination, consolidation support, and reporting.

Companies often outsource repeatable, rules-based work such as balance sheet reconciliations, journal support, close calendar management, intercompany matching, and routine reporting. Final sign-off, accounting policy decisions, and high-risk judgments usually stay in-house.

It speeds up the close by standardizing workflows, clarifying ownership, and enforcing deadlines across entities and tasks. This reduces delays caused by missing support, late reconciliations, and inconsistent review practices.

Staff augmentation adds people, but your team still manages the process design, training, and control consistency. Record to report outsourcing transfers a defined scope of work with service levels, governance, and clearer accountability.

It helps address slow closes, reconciliation backlogs, fragmented controls, poor visibility into close status, and rising finance overhead. It can also reduce burnout by shifting repetitive accounting work away from internal leaders.

Product Trial

FineReport

Pixel-perfect reports · Interactive dashboards · Easy data entry · Digital twins