International financial reporting standards matter most when an enterprise finance team must close faster, report consistently across entities, satisfy auditors, and explain results to global stakeholders without reconciling multiple accounting languages every quarter. For controllership leaders, finance directors, and group reporting teams, IFRS is not just a technical accounting topic. It is an operating model issue that affects policy decisions, ERP configuration, consolidation logic, disclosures, covenant reporting, and investor confidence.

Click To Try The Dashboard

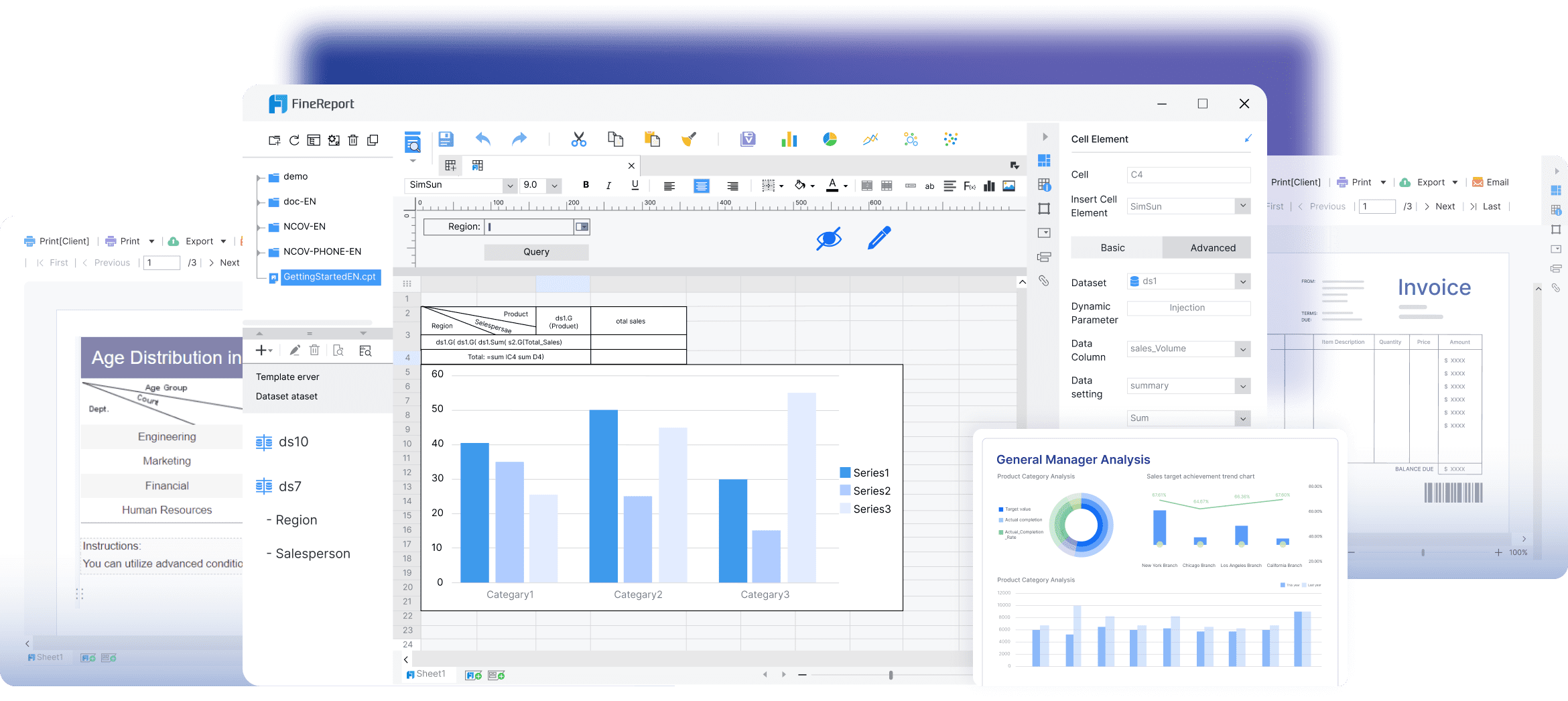

All reports in this article are built with FineReport

What are international financial reporting standards?

International financial reporting standards are a globally recognized set of accounting standards used to prepare financial statements in a consistent, transparent, and comparable way across countries and markets. In plain language, IFRS gives enterprise finance teams a common framework for deciding how revenue, leases, financial instruments, impairments, consolidation, and disclosures should appear in the financial statements.

For large organizations, the core value of IFRS is comparability. If your business operates through multiple subsidiaries, legal entities, or jurisdictions, leadership needs financial statements that can be understood on a like-for-like basis. Investors, lenders, audit committees, and regulators also want numbers they can compare across peers and across periods without decoding local accounting differences in every report.

IFRS is designed to produce financial statements that are decision-useful. That means the output should help users assess performance, financial position, risks, and future cash flow implications. This is especially important in cross-border environments where capital providers need a clear view of enterprise economics.

In practice, the main users of IFRS reporting include:

Multinational companies that need a common reporting framework across subsidiaries

Investors and analysts comparing companies across regions

Finance leaders and boards making capital allocation, performance, and risk decisions

Key Metrics (KPIs) finance teams should monitor in an IFRS environment

A strong IFRS reporting process depends on operational and governance metrics, not just final financial statement outputs. The most useful KPIs include:

Close cycle time: Measures how quickly the group can finalize IFRS numbers after period end.

Adjustment volume: Tracks the number and value of manual journal entries, reclasses, and top-side adjustments.

Policy exception rate: Shows how often subsidiaries deviate from approved IFRS accounting policies.

Disclosure completeness: Measures progress against required note disclosures and supporting schedules.

Intercompany elimination accuracy: Assesses the quality of intercompany matching and consolidation eliminations.

Lease data completeness: Monitors whether all lease contracts and reassessments are captured for IFRS 16.

Impairment trigger coverage: Tracks whether all reporting units or cash-generating units have been assessed.

Fair value model validation status: Confirms review and approval of valuation methods and assumptions.

Audit issue resolution time: Measures how quickly finance closes open review points raised by internal or external auditors.

How IFRS works in practice

IFRS does not run itself. Enterprise teams must convert high-level standards into policies, controls, master data, review checkpoints, and reporting workflows. That is where many finance transformations either succeed or stall.

The role of the IFRS Foundation and the IASB

The IFRS Foundation provides the governance and oversight structure that supports the IFRS system. Within that structure, the International Accounting Standards Board, or IASB, is the independent body responsible for developing and issuing IFRS Accounting Standards.

For finance teams, the distinction matters:

The IFRS Foundation oversees governance, due process, and institutional support

The IASB develops, updates, and amends the accounting standards themselves

New standards and amendments are not created overnight. They typically move through consultation, exposure drafts, stakeholder feedback, redeliberation, and final issuance. That means enterprise reporting teams need a disciplined process to monitor what is effective now, what is changing next, and what disclosures may be required before full implementation.

One of the defining features of international financial reporting standards is that they are principle-based. Instead of prescribing an answer for every narrow scenario, IFRS sets out broad principles that companies must apply using professional judgment.

This gives finance teams flexibility, but it also raises the bar for documentation, review, and governance. The goal is not just technical compliance. The goal is to reflect the economic substance of transactions faithfully.

Key principles include:

Materiality: Information should be included if omitting or misstating it could influence user decisions.

Faithful representation: Financial information should be complete, neutral, and free from material error.

Consistency: Similar transactions should be treated in a consistent way across periods and entities unless a justified change is approved.

Transparency through disclosure: When judgment, estimation, or uncertainty is significant, disclosures must clearly explain it.

For enterprise teams, these principles affect everyday reporting decisions. For example, determining whether a contract contains a lease, identifying performance obligations in bundled revenue contracts, or assessing expected credit losses all require sound judgment backed by evidence.

What a finance team must do to apply IFRS

Applying IFRS is an enterprise process, not an accounting memo. A finance team must operationalize the standards across policy design, transaction processing, reporting controls, and disclosure management.

In practical terms, this usually means the team must:

Convert IFRS requirements into formal accounting policies

Define control activities for judgment-heavy areas

Map required inputs to ERP, subledger, and consolidation data fields

Build period-end workflows for review, approval, and disclosure drafting

Maintain supporting documentation for auditors and regulators

Cross-functional coordination is essential. IFRS application often depends on information that sits outside controllership:

Tax may affect deferred tax treatment and uncertain positions

Treasury influences debt classification, hedging, and covenant reporting

Legal interprets contract terms relevant to revenue, leases, and contingencies

Procurement and operations hold source data for embedded leases and commitments

IT and systems teams must enable required data capture and reporting logic

Global organizations adopt or report under IFRS because fragmented accounting frameworks create friction. When each country, business unit, or acquisition reports differently, group finance spends more time reconciling than analyzing.

Benefits for multinational reporting and cross-border stakeholders

For multinational groups, IFRS improves comparability across subsidiaries and jurisdictions. That helps headquarters evaluate performance using a more consistent basis, especially where legal entities operate under different local reporting traditions.

The benefits are practical and strategic:

Cleaner group consolidation with fewer framework-driven adjustments

More consistent board reporting across business units

Better communication with investors and lenders who compare issuers globally

Stronger support for M&A integration when newly acquired entities must align to group policies

Improved confidence in performance metrics used for planning and capital allocation

When capital providers review a company with international operations, they want transparency on how earnings are generated, how liabilities are measured, and how risks are disclosed. IFRS helps provide that common baseline.

Common challenges during adoption and ongoing compliance

The main challenge is that IFRS adoption is rarely just a standards exercise. It usually triggers process redesign, system remediation, training programs, and governance changes.

Common pain points include:

Transition complexity when legacy policies differ from IFRS requirements

Training demands for finance staff, local controllers, and non-finance stakeholders

Systems changes to capture new data attributes and calculation logic

Judgment-heavy areas where different teams may initially interpret standards inconsistently

Disclosure burden that expands beyond the trial balance

Tension between global IFRS reporting and local statutory rules

This last point is critical. A group may report under IFRS centrally while subsidiaries still need local GAAP or statutory reporting. That creates dual-reporting pressure unless the finance architecture is designed to manage both efficiently.

Navigating International Financial Reporting Standards in key reporting areas

Not all standards create the same level of effort. In most enterprises, a small number of reporting areas drive most of the complexity, audit attention, and disclosure volume.

Revenue, leases, and financial instruments

These are three of the highest-impact areas in IFRS reporting because they directly affect earnings patterns, liabilities, forecasts, and investor messaging.

Revenue requires teams to assess contracts, identify performance obligations, determine transaction prices, and decide when control transfers. This can materially change timing of revenue recognition, especially in complex service, bundled, milestone, or multi-element arrangements.

Leases affect both the balance sheet and key ratios. Under IFRS 16, most leases are brought onto the balance sheet, which means finance teams need reliable contract inventories, discount rate logic, reassessment controls, and right-of-use asset tracking.

Financial instruments often demand careful classification, impairment modeling, hedge documentation, and fair value measurement. Even companies outside financial services can face complexity through receivables, debt, investments, guarantees, and treasury instruments.

Consolidation, impairment, and fair value measurement

Large enterprise groups often face the hardest IFRS questions in consolidation scope, impairment testing, and fair value estimation.

Consolidation issues arise when the group must determine control, treatment of structured entities, intercompany eliminations, and consistency of subsidiary accounting policies. Acquisitions and partial ownership structures add more complexity.

Impairment requires rigorous assumptions, trigger assessments, cash flow forecasts, discount rates, and sensitivity analysis. It is one of the most judgment-sensitive areas in group reporting and frequently receives intense audit review.

Fair value measurement becomes critical where assets or liabilities depend on market inputs, models, or valuation specialists. The finance team must ensure methodologies are consistent, assumptions are documented, and governance is strong.

In all three areas, audit readiness depends on disciplined evidence management. Strong teams do not wait until year-end to assemble support. They maintain version control, approval trails, model documentation, and review records throughout the reporting cycle.

Building an IFRS-ready finance function

An IFRS-ready finance function is one that can absorb change, apply judgment consistently, and produce reliable outputs under pressure. That requires governance, systems alignment, and repeatable execution.

Creating an implementation roadmap

If your organization is adopting IFRS for the first time, expanding into new jurisdictions, or upgrading its reporting process, start with a structured roadmap.

Here is the approach I recommend as a consultant:

Run a gap assessment

Compare current accounting policies, disclosures, systems, and close workflows against IFRS requirements.

Identify the highest-risk standards first, especially revenue, leases, financial instruments, and consolidation.

Design target policies and governance

Create group accounting papers that define required treatments, elections, thresholds, and documentation standards.

Establish approval owners, escalation paths, and policy version control.

Assess systems and data readiness

Confirm whether ERP, lease tools, consolidation platforms, and reporting models capture the required inputs.

Eliminate spreadsheet dependencies where they create control risk.

Build training by role

Train not just technical accountants, but local finance teams, legal reviewers, treasury, and system owners.

Use scenario-based examples tied to actual contracts and reporting issues.

Pilot before full rollout

Test the process with selected entities or reporting areas before group-wide deployment.

Refine controls, templates, and instructions based on pilot issues.

Strengthening reporting quality over time

IFRS readiness is not a one-time project. Standards evolve, business models change, and transactions become more complex. Mature finance teams build recurring review routines rather than treating compliance as an annual event.

Best practices that consistently improve reporting quality include:

Conducting quarterly policy reviews for new standards and amendments

Maintaining a disclosure calendar with accountable owners

Running pre-close judgment reviews for high-risk estimates and unusual transactions

Aligning FP&A, controllership, internal audit, and external advisors on key assumptions early

Tracking recurring audit findings and converting them into process improvements

When these routines are embedded, finance becomes faster, more defensible, and more trusted by leadership.

After best practices are defined, teams usually reach the same conclusion: manual execution is possible, but it is slow, hard to scale, and vulnerable to control gaps.

Not always. The core international financial reporting standards are global, but adoption and endorsement can vary by jurisdiction. Some countries adopt IFRS largely as issued, while others use endorsement mechanisms, local carve-outs, or additional regulatory overlays.

For enterprise finance teams, the practical takeaway is simple: never assume that “IFRS” means the exact same legal reporting framework in every country where you operate. Group policy teams should verify local requirements and map any differences into the reporting model.

How is IFRS different from other accounting frameworks?

At a high level, IFRS is known for its principle-based approach, while some other frameworks, most notably US GAAP, are often seen as more rules-based. That means IFRS generally relies more heavily on professional judgment and on explaining the economic substance of transactions.

A practical comparison looks like this:

IFRS: Broader principles, more judgment, strong focus on comparability and transparency

US GAAP: More detailed guidance in many areas, often more prescriptive in application

Local GAAP frameworks: May be narrower, tax-driven, or more focused on statutory reporting than investor comparability

For most enterprise teams, the real issue is not academic difference. It is operational impact: policy mapping, system configuration, disclosures, and reconciliations.

When should an enterprise finance team seek outside support?

Outside support makes sense when the reporting risk is high, timelines are tight, or the transaction is unusual. Common triggers include:

First-time IFRS adoption

Major acquisitions, disposals, or restructurings

ERP or consolidation system transformation

Complex revenue arrangements or lease populations

Fair value and impairment assessments

High-stakes judgments likely to attract audit or regulatory scrutiny

External specialists can help accelerate policy decisions, challenge assumptions, improve documentation, and reduce rework during close and audit cycles.

Turn IFRS methodology into an automated reporting workflow with FineReport

Building this manually is complex; use FineReport to utilize ready-made templates and automate this entire workflow. For enterprise finance teams, the challenge is not just understanding international financial reporting standards. It is turning policy requirements into repeatable dashboards, disclosure schedules, entity submissions, reconciliation packs, and management-ready reports.

FineReport helps bridge that gap by enabling teams to:

Centralize IFRS reporting inputs from multiple systems

Build standardized reporting templates for entities and group finance

Automate recurring dashboards for close, consolidation, and disclosure tracking

Improve control visibility with workflow-based approvals

That matters when finance leaders need real-time visibility into close status, reporting exceptions, adjustment trends, and audit readiness across the group.

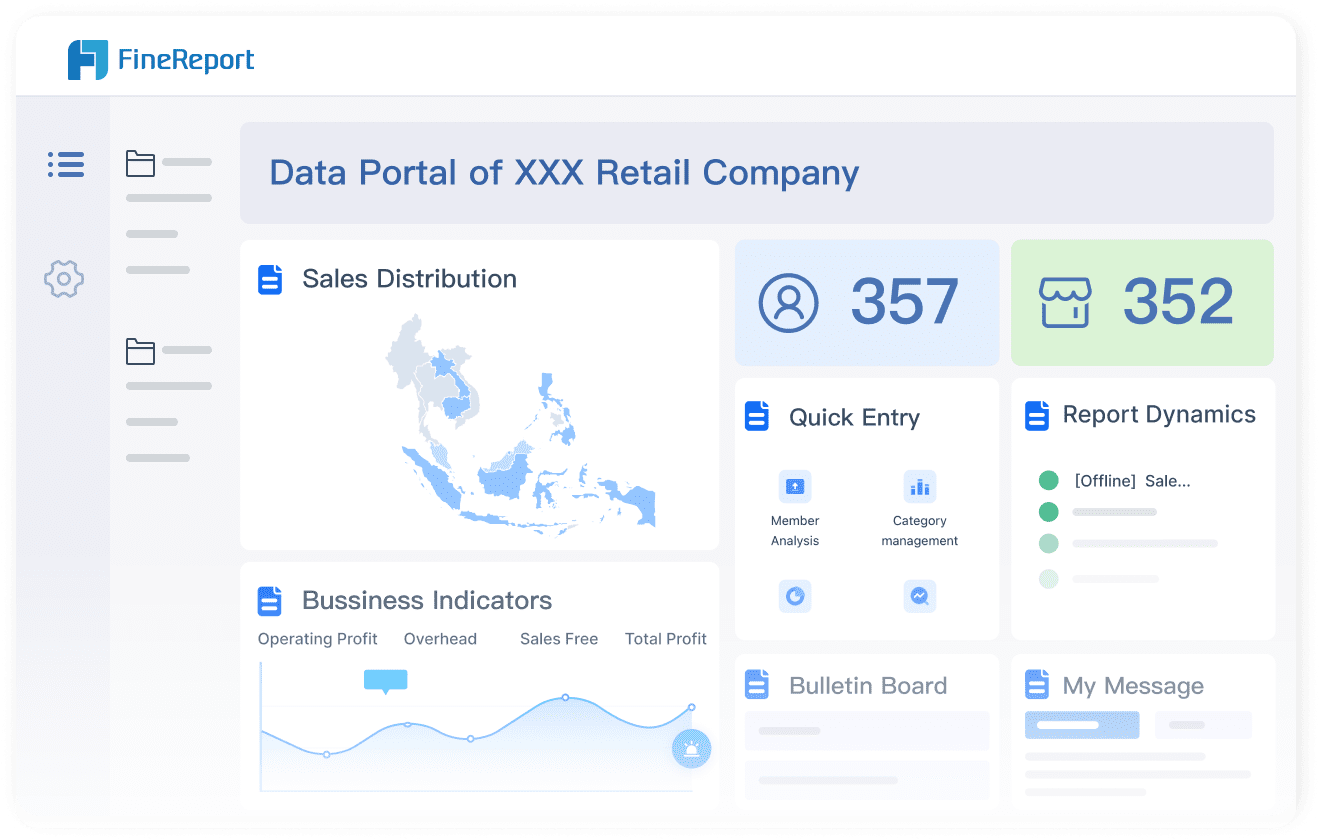

Get Ready-to-Use Dashboard Templates in Fine Gallery

If your team is standardizing IFRS reporting, preparing for expansion, or trying to reduce manual consolidation and disclosure work, this is the point where better tooling changes the economics of the process.

IFRS gives finance teams a common accounting framework so financial statements are consistent, transparent, and comparable across entities and jurisdictions. This helps management, investors, auditors, and regulators interpret results more reliably.

IFRS Accounting Standards are developed and issued by the IASB. The IFRS Foundation provides the governance, oversight, and due process structure that supports that standard-setting work.

IFRS is generally principles-based, which means it relies more on professional judgment and broader guidance. US GAAP is often more rules-based and includes more detailed requirements for specific scenarios.

Multinational groups need a consistent reporting language across subsidiaries, currencies, and local accounting environments. IFRS improves consolidation, reduces reporting friction, and supports clearer communication with global stakeholders.

The biggest effort usually comes from turning standards into practical policies, controls, data structures, and review workflows. Revenue recognition, leases, financial instruments, impairments, consolidation, and disclosures often require the most coordination.

Product Trial

FineReport

Pixel-perfect reports · Interactive dashboards · Easy data entry · Digital twins