Financial reporting compliance terminology is the shared language finance teams use to prepare accurate statements, meet filing deadlines, document controls, and communicate clearly with auditors, regulators, and executives. For controllers, finance managers, accounting leads, and compliance teams, inconsistent wording creates real operational risk: review delays, incomplete support, control gaps, duplicated work, and avoidable audit friction. A clear, standardized glossary helps teams align faster, document better, and reduce reporting errors across the close, audit, and filing cycle.

Click To Try The Dashboard

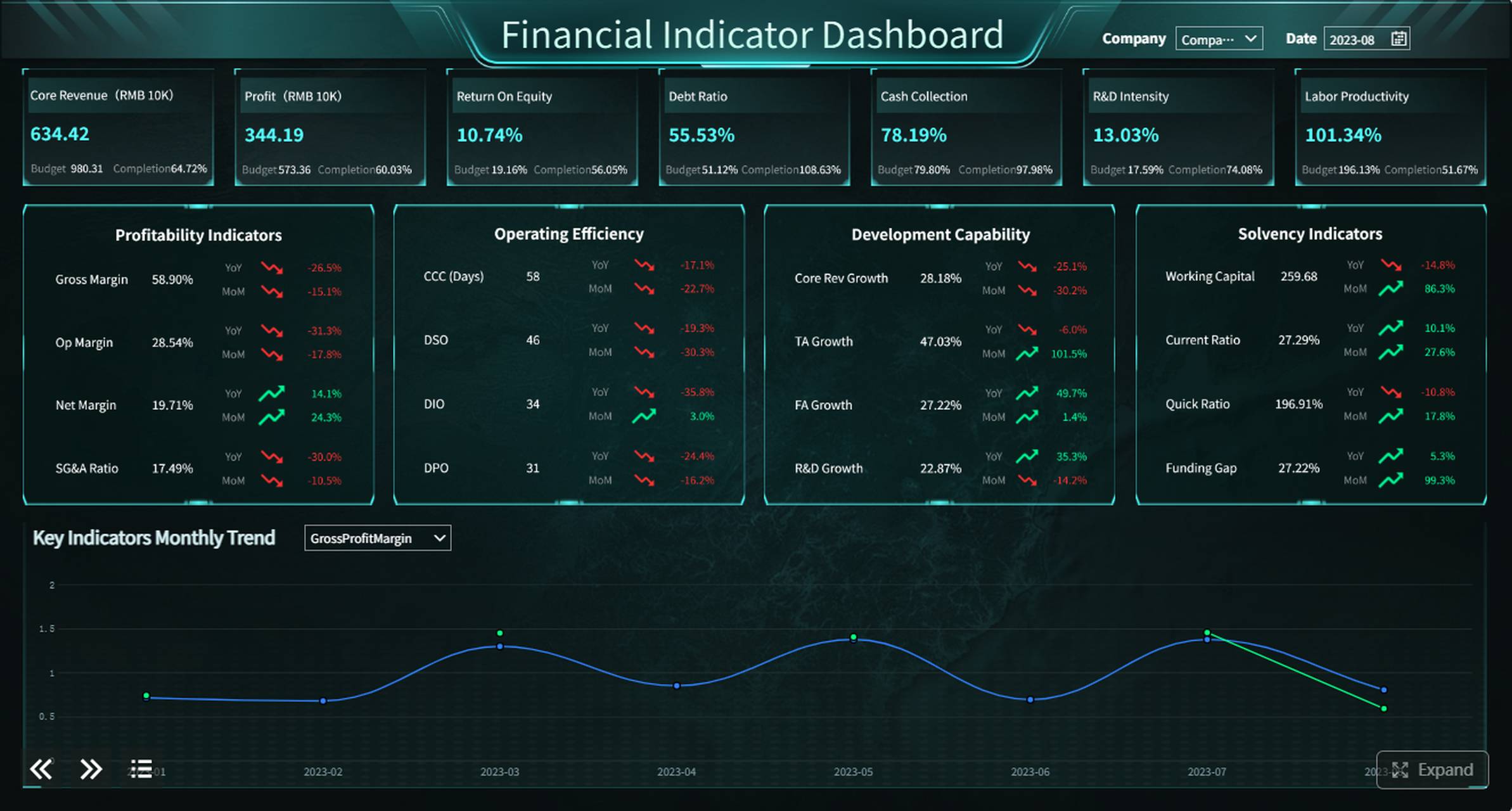

All reports in this article are built with FineReport

What Financial Reporting Compliance Terminology Means for Finance Teams

Financial reporting compliance terminology refers to the standardized words and definitions used across accounting, external reporting, internal control, audit, and governance activities. In plain language, it is the vocabulary that tells everyone what must be reported, how it should be reviewed, who owns each step, and what evidence is needed to prove compliance.

For finance teams, shared terminology is not just a documentation exercise. It directly affects how quickly issues are resolved and how confidently reports are issued. When one team says “exception,” another says “deficiency,” and a third says “open item,” confusion builds fast. That confusion can affect reconciliations, sign-offs, audit responses, and filings.

A common vocabulary improves four critical outcomes:

Accuracy: Teams apply the same definitions to balances, disclosures, and control conclusions.

Timeliness: Close tasks, review comments, and escalation paths become easier to manage.

Control reliability: Staff know the difference between a control gap, a deficiency, and a material weakness.

Regulatory communication: Filings, memos, and responses use precise language that stands up to scrutiny.

This glossary is also useful beyond the reporting cycle. Finance leaders can use it for:

Onboarding new hires into reporting and compliance responsibilities

Cross-functional training for legal, operations, tax, and investor relations teams

Review readiness before month-end, quarter-end, annual audit, or regulatory filing

Core Financial Reporting and Compliance Terms

Reporting framework and standard-setting terms

At the foundation of financial reporting compliance terminology is the reporting framework. This is the rulebook that governs how transactions are recognized, measured, presented, and disclosed.

Key concepts include:

GAAP: Generally Accepted Accounting Principles, commonly used in the United States

IFRS: International Financial Reporting Standards, used in many jurisdictions outside the U.S.

Reporting framework: The formal set of accounting standards and principles an entity follows

Accounting policy: Management’s chosen method for applying accounting standards to specific transactions

Materiality: The threshold at which an omission or misstatement could influence user decisions

Teams must also understand the difference between three often-mixed concepts:

A standard sets formal accounting requirements

An interpretation clarifies how a standard should be applied in practice

An internal policy translates the standard into company-specific procedures and decision rules

This distinction matters because audit issues often arise not from the standard itself, but from weak internal policy translation or inconsistent application across business units.

Filing, disclosure, and documentation terms

Financial reporting is not complete when numbers are finalized. It is complete when those numbers are properly disclosed, documented, and filed according to regulatory requirements.

Important terms in this category include:

Disclosure: Required narrative or quantitative information accompanying the financial statements

Footnotes: Detailed notes that explain accounting policies, estimates, risks, and line items

Management representation: Formal written statements from management asserting responsibility for the financial statements and related information

Supporting documentation: Evidence that backs reported balances, disclosures, and judgments

Filing requirements: Legal or regulatory rules governing what must be submitted, when, and in what format

Strong documentation is what turns a reported number into a defensible position. Without it, teams struggle during review, external audit, or regulator follow-up.

Control and assurance terms

Compliance depends on more than accounting knowledge. It depends on controls that prevent, detect, and correct errors.

Core control and assurance terms include:

Internal control: A process designed to provide reasonable assurance over reporting reliability and compliance

Segregation of duties: Splitting responsibilities so one person does not control an entire high-risk process

Control deficiency: A weakness in the design or operation of a control

Remediation: Corrective action taken to resolve a control issue

Audit trail: The record showing how data moved, changed, and was approved

Assurance: Confidence provided through testing, review, or audit that information is reliable

These terms are tightly linked. A missing review step may create a control deficiency. If unresolved, it may weaken assurance over reported numbers. If severe enough, it may trigger disclosure or escalation.

45 Essential Terms Every Finance Team Should Know

To help finance leaders build a practical internal glossary, below are 45 essential terms grouped by use case.

Terms tied to accuracy and completeness

Reconciliation — The process of comparing two sets of records to confirm they agree and investigating differences.

Adjusting entry — A journal entry made to correct, allocate, or update balances before statements are finalized.

Cutoff — The rule for recording transactions in the correct reporting period.

Completeness — The assertion that all required transactions, balances, and disclosures are included.

Valuation — The assertion that assets, liabilities, revenues, and expenses are recorded at appropriate amounts.

Classification — The correct presentation of items in the proper accounts and statement lines.

Consistency — Applying accounting methods the same way across periods unless a justified change is disclosed.

Occurrence — The assertion that recorded transactions actually happened and relate to the entity.

Existence — The assertion that reported assets or liabilities truly exist at the reporting date.

Accuracy — The degree to which amounts and related data are recorded correctly.

Estimate — A judgment-based amount used when precise measurement is not possible.

Accrual — Recognition of revenue or expense when earned or incurred, not necessarily when cash moves.

Common confusion points include accuracy vs completeness, cutoff vs accrual, and classification vs valuation. Misusing these terms often leads to vague review notes and incomplete corrective actions.

Governance — The structure of oversight, decision-making, and accountability around reporting and compliance.

Sign-off — Formal confirmation that a task, reconciliation, or report has been reviewed and approved.

Review — A supervisory examination of work for reasonableness, completeness, and compliance.

Certification — A formal attestation that information is accurate and controls or procedures have been followed.

Escalation — Raising an issue to a higher authority because of risk, impact, or unresolved status.

Exception — An item that falls outside expected rules, thresholds, or approved conditions.

Oversight — Ongoing monitoring by management, committees, or boards over reporting quality and compliance.

Ownership — Clear assignment of responsibility for a process, control, or deliverable.

Accountability — The obligation to answer for results, decisions, and unresolved issues.

Approval matrix — A defined structure showing who can review, approve, or escalate decisions.

Typical owners vary by company, but finance managers often own review, controllers own sign-off discipline, executive leadership owns certification, and audit committees provide oversight.

Terms tied to risk, audit, and enforcement

Audit scope — The boundaries of what the audit covers, including entities, periods, processes, and accounts.

Sampling — Testing a subset of items to draw conclusions about a larger population.

Evidence — Documentation or data used to support an accounting conclusion or audit finding.

Noncompliance — Failure to follow an applicable law, regulation, policy, or reporting requirement.

Restatement — Reissuance or correction of prior financial statements due to material error or misapplication.

Deficiency — A problem in a control that reduces its ability to prevent or detect misstatements.

Significant deficiency — A deficiency serious enough to merit attention by those charged with governance.

Material weakness — A deficiency, or combination of deficiencies, creating a reasonable possibility of material misstatement.

Enforcement action — A formal regulatory response to violations, such as penalties, orders, or required corrections.

Risk assessment — The process of identifying and evaluating reporting risks and their potential impact.

Fraud risk — The possibility that intentional misstatement or misappropriation affects reporting.

Control testing — Procedures performed to verify that controls are designed effectively and operating as intended.

Substantive testing — Audit procedures focused directly on balances, transactions, and disclosures.

These are high-signal terms. When a discussion shifts from issue to deficiency, or from deficiency to material weakness, the risk level has materially changed and governance attention should increase.

Terms tied to deadlines and reporting cycles

Reporting period — The time span covered by the financial statements.

Close calendar — The schedule of tasks, dependencies, owners, and due dates for the reporting cycle.

Filing deadline — The required date by which a report must be submitted to the relevant authority.

Subsequent events — Events occurring after period-end but before issuance that may require disclosure or adjustment.

Issuance date — The date financial statements are formally released or made available.

Amendment — A formal revision to a previously filed or issued report.

Tick and tie — The process of verifying that amounts agree across statements, notes, and supporting schedules.

Open item log — A tracked list of unresolved issues, requests, or pending documentation.

Prepared-by client (PBC) — Documents and schedules requested by auditors from management.

Close checklist — A standardized list of required tasks to complete the reporting process.

Key Metrics (KPIs)

To operationalize financial reporting compliance terminology, finance teams should track these KPIs consistently:

Close cycle time — Number of days required to complete the monthly or quarterly close.

On-time filing rate — Percentage of reports submitted by the filing deadline.

Reconciliation completion rate — Percentage of reconciliations completed, reviewed, and approved on time.

Open exceptions count — Total number of unresolved reporting or control exceptions.

Control deficiency rate — Number of deficiencies identified within a reporting cycle or testing period.

Remediation cycle time — Average time required to close a deficiency after identification.

Audit request turnaround time — Time taken to fulfill auditor or regulator information requests.

Documentation completeness rate — Percentage of balances, disclosures, or controls with full supporting evidence.

Review rework rate — Percentage of submissions returned for correction after review.

Restatement incidence — Number of corrections or restatements over a defined period.

How to Use Compliance Terminology in Day-to-Day Reporting

During the monthly and quarterly close

The close is where terminology discipline pays off immediately. Every reconciliation, checklist item, review note, and issue log should use consistent labels. If teams document a problem as an exception, they should define whether it is a timing issue, support gap, control failure, or potential misstatement.

Best practice is to standardize the language used in:

Reconciliation templates

Journal entry support

Review comments

Open item logs

Close calendars

Escalation trackers

This reduces rework because reviewers do not need to reinterpret what preparers meant. It also speeds approvals, since ownership and severity are easier to identify.

During audits and regulator-facing work

Precise wording matters even more when communicating externally. Audit requests, PBC lists, remediation plans, and disclosure drafts should avoid vague phrases like “issue under review” when a more accurate label exists.

Use terminology that answers three questions clearly:

What happened? Example: control deficiency, cutoff error, incomplete documentation

What is the impact? Example: no material misstatement identified, disclosure update required, testing expanded

What is the response? Example: remediation initiated, escalation completed, amendment under evaluation

Clear language improves evidence tracking, speeds request resolution, and reduces unnecessary back-and-forth with auditors and regulators.

During training and cross-functional communication

A financial reporting compliance terminology glossary should not stay inside accounting. Legal, operations, procurement, HR, tax, internal audit, and executives all influence reporting inputs and control performance.

To make the glossary practical:

Include it in onboarding for finance and adjacent functions

Link terms to real company workflows and templates

Review terms before quarter-end and annual reporting cycles

Update definitions when standards, policies, or control owners change

Use the same language in dashboards, status meetings, and written memos

When everyone uses the same terminology, cross-functional friction drops and reporting confidence rises.

Commonly Confused Financial Reporting Terms

Some financial reporting compliance terminology looks similar but carries very different implications. These distinctions matter during close, audit, and filing preparation.

Error vs fraud

An error is unintentional. Fraud involves intentional deception. Rule of thumb: if intent is unclear, avoid assumptions and escalate based on facts.

Policy vs estimate

A policy is the method the company chooses to follow. An estimate is the amount determined using judgment within that method. Rule of thumb: policy answers “how,” estimate answers “how much.”

Review vs audit

A review generally provides limited assurance through inquiry and analytical procedures. An audit provides higher assurance through broader testing and evidence gathering. Rule of thumb: not every review is an audit, and teams should not use the terms interchangeably.

Deficiency vs material weakness

A deficiency is a control problem. A material weakness is a severe control problem with a reasonable possibility of material misstatement. Rule of thumb: every material weakness is a deficiency, but not every deficiency is a material weakness.

Exception vs noncompliance

An exception is a deviation from an expected result or rule. Noncompliance means a requirement was actually not met. Rule of thumb: exceptions may require investigation; noncompliance usually requires response and correction.

Cutoff vs subsequent events Cutoff addresses whether a transaction belongs in the correct period. Subsequent events concern events after period-end that may affect reporting before issuance. Rule of thumb: cutoff is about transaction timing; subsequent events are about post-period developments.

Supporting documentation vs evidence Supporting documentation is the recorded backup. Evidence is the broader proof used to support a conclusion, which may include documentation, confirmations, system logs, or approvals. Rule of thumb: all supporting documentation can be evidence, but evidence is broader.

Quick rules like these help teams write more precise memos, cleaner checklists, and more defensible status updates.

Building a Stronger Reporting Process Through Shared Language

Consistent financial reporting compliance terminology improves more than communication. It strengthens accountability, supports internal control discipline, reduces review friction, and increases the quality of financial statements. Teams that define terms clearly are better prepared to manage close calendars, document judgments, support disclosures, respond to auditors, and meet filing deadlines without last-minute confusion.

From a consulting perspective, the most effective organizations do three things well:

Standardize definitions across templates, workflows, and approvals

Assign ownership for terms tied to controls, disclosures, and escalations

Review and update the glossary as standards, regulations, and processes evolve

Actionable best practices for implementation

If you want to operationalize this terminology across the reporting process, start here:

Store the glossary in a shared location with version control.

Require finance leaders to approve changes.

Embed terminology into core workflows

Add standardized term selections to reconciliation templates, close checklists, issue logs, and remediation trackers.

Use dropdown fields where possible to reduce wording inconsistencies.

Align dashboard labels with the same glossary definitions.

Train by scenario, not by theory

Run short workshops using examples from the monthly close, external audit, and filing review.

Ask teams to classify issues using approved terms.

Correct ambiguous wording before it appears in formal reporting.

Link terms to governance and escalation

Define which terms trigger controller review, executive sign-off, legal input, or audit committee visibility.

Set thresholds for when an exception becomes a deficiency or when remediation requires escalation.

Make ownership explicit for each step.

Measure terminology adoption

Review issue logs and close packages for inconsistent wording.

Track rework caused by unclear review comments or poorly labeled exceptions.

Use recurring errors to refine training and glossary definitions.

Building this manually is complex; use FineReport to utilize ready-made templates and automate this entire workflow.

Get Ready-to-Use Dashboard Templates in Fine Gallery

With FineReport, finance teams can centralize definitions, standardize reporting dashboards, track close and filing KPIs, monitor exceptions, and present audit-ready information in a consistent format. Instead of stitching together spreadsheets, emails, and disconnected trackers, teams can automate status visibility and improve governance across the reporting cycle.

An internal glossary should be treated like a living control document. Revisit it when accounting standards change, filing requirements shift, new systems are introduced, or ownership moves across teams. The goal is simple: make sure every person involved in financial reporting uses the same language to describe the same risk, action, and decision.

It is the set of standardized terms finance teams use to prepare reports, document controls, support disclosures, and communicate with auditors and regulators. A shared vocabulary helps reduce confusion and improves reporting consistency.

Consistent wording helps teams align on ownership, evidence, review status, and control issues. This reduces delays, audit friction, and the risk of reporting errors.

A reporting framework is the overall rulebook, such as GAAP or IFRS, that governs financial reporting. An accounting policy is the company’s chosen method for applying those rules to specific transactions or situations.

A control deficiency is a problem in the design or operation of a control. A material weakness is a more serious issue that creates a reasonable possibility of a material misstatement in the financial statements.

Common support includes reconciliations, review sign-offs, disclosure backup, policy memos, audit trails, and management representations. These records help prove that balances, judgments, and filings are accurate and properly reviewed.

Product Trial

FineReport

Pixel-perfect reports · Interactive dashboards · Easy data entry · Digital twins