CSRD reporting is the operating model enterprises need to turn sustainability disclosure into a controlled, auditable business process. For finance leaders, sustainability teams, legal counsel, and internal audit, the challenge is not just understanding the rulebook. It is determining scope across entities, interpreting ESRS requirements, running a defensible double materiality assessment, and producing disclosures that can stand up to assurance. If your organization has EU operations, listed entities, or meaningful European revenue, getting CSRD reporting right can reduce compliance risk, improve investor confidence, and strengthen enterprise governance.

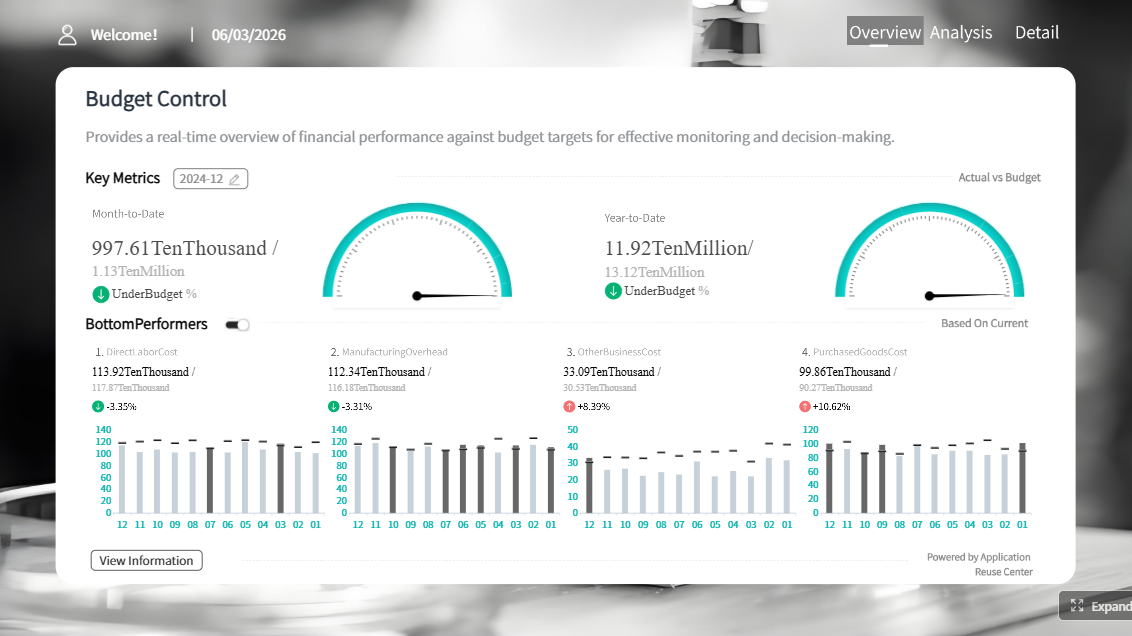

Click To Try The Dashboard

All reports in this article are built with FineReport

CSRD reporting refers to the sustainability disclosure obligations introduced by the Corporate Sustainability Reporting Directive. In practical terms, it requires organizations in scope to report standardized information about how sustainability issues affect the business and how the business affects people and the environment. This is not a side report for communications teams. It is a regulated reporting exercise that touches finance, operations, procurement, HR, risk, and IT.

For enterprise teams, the business value is clear. Strong CSRD reporting creates a more reliable view of sustainability risks, operational dependencies, transition plans, and value chain exposure. It also helps management respond to growing demands from investors, customers, regulators, lenders, and boards.

CSRD reporting matters because it expands sustainability disclosure far beyond earlier EU requirements. Compared with previous frameworks, it is broader in scope, more structured in content, more integrated with management reporting, and more demanding in terms of controls and auditability. That means many companies must move from narrative ESG reporting to a governed reporting process with clear ownership, evidence, and review cycles.

Global companies should pay attention even if they are not headquartered in the EU. A non-EU parent may still be affected through EU subsidiaries, branches, listings, or revenue thresholds. For multinational groups, the real issue is not geography alone. It is how the legal structure, consolidation perimeter, and EU footprint interact with the rule.

Key Metrics (KPIs) for CSRD reporting readiness

Entity scope coverage: Percentage of legal entities assessed for CSRD applicability.

Reporting boundary completeness: Degree to which subsidiaries, branches, and value chain considerations are mapped.

ESRS disclosure readiness: Share of required disclosures with assigned owners, data sources, and draft content.

Double materiality completion rate: Progress of stakeholder input, topic scoring, validation, and documentation.

Data source maturity: Percentage of required data points linked to reliable systems or controlled manual processes.

Control coverage: Portion of critical disclosures supported by documented review and approval controls.

Evidence traceability: Extent to which disclosures can be tied back to source records and supporting documentation.

Assurance readiness: Percentage of disclosures prepared to withstand limited assurance procedures.

Policy alignment rate: Share of relevant sustainability policies updated to reflect reported commitments and actions.

Board oversight cadence: Frequency and completeness of executive and board review of CSRD reporting progress.

Who is in scope and when reporting starts

Determining scope is the first make-or-break step in CSRD reporting. Many organizations waste months collecting data before confirming which entities are actually covered. The right approach is to assess applicability at group and entity level, then align that scope with reporting boundaries, governance, and timelines.

CSRD reporting generally applies to categories such as EU-listed entities, large companies, and certain non-EU businesses with significant EU activity. In practice, this requires a structured assessment of corporate form, listing status, employee and financial thresholds, and the presence of qualifying EU subsidiaries or branches.

For enterprise groups, group structures matter. A parent may not assess scope the same way as a subsidiary. Some entities may be captured because they are listed. Others may fall in based on size or consolidated status. That means the reporting boundary cannot be determined from one legal test alone. You need to evaluate how local entity obligations and group reporting interact.

Subsidiaries also need careful review. In some cases, a subsidiary may rely on group-level reporting arrangements, while in others it may still need separate consideration. The operational takeaway is simple: build a scope memo for every material entity, document assumptions, and have legal and finance validate the perimeter.

Key timelines and phase-in dates

Implementation has been phased in over multiple filing waves, and each reporting year has practical consequences for project planning. The first wave of organizations began with earlier financial years, while later waves bring additional large entities and some non-EU groups into focus over time.

For management teams, the important point is not memorizing every date. It is understanding backward planning. If your first mandatory report is approaching, the heavy lifting must start well before year-end. Scope assessments, materiality, control design, and data architecture cannot be left to the reporting quarter.

Early preparation reduces three major risks:

Data risk: Missing source systems, manual gaps, and inconsistent definitions.

Governance risk: Unclear ownership, fragmented workflows, and delayed approvals.

Assurance risk: Weak evidence trails, undocumented judgments, and unreliable calculations.

What US companies need to know

US-headquartered companies often assume CSRD reporting is a European issue. That is a costly mistake. If your group has EU subsidiaries, listed EU entities, or significant EU-generated business activity, your organization may still be captured directly or indirectly.

The practical implications are cross-functional:

Legal teams must interpret applicability across entities and jurisdictions.

Finance teams must build controls, consolidation logic, and reporting calendars.

Sustainability teams must translate business impacts and risks into ESRS-aligned content.

Internal audit must evaluate process design, evidence quality, and assurance preparedness.

For US enterprises, the toughest challenge is usually integration. Sustainability data often sits outside the financial reporting infrastructure. CSRD reporting forces those functions together, which means systems, governance, and accountability need to mature quickly.

Understanding ESRS and what must be disclosed

The European Sustainability Reporting Standards, or ESRS, are the reporting backbone of CSRD reporting. They define what organizations must disclose, how topics are structured, and how narrative statements connect to metrics, targets, policies, and actions. If CSRD is the legal obligation, ESRS is the operating language.

The ESRS framework is organized into cross-cutting standards and topical standards spanning environmental, social, and governance matters. The cross-cutting standards establish general principles and overarching disclosure concepts. The topical standards then go deeper into subject areas such as climate, pollution, water, biodiversity, workforce, affected communities, consumers, and business conduct.

For enterprise teams, the critical shift is this: disclosure requirements are not just broad topics. They break down into specific reporting obligations and data points. That means each required disclosure must be translated into:

Without that translation layer, organizations end up with theoretical compliance plans that collapse during drafting and assurance.

Core disclosure areas to prepare for

Most CSRD reporting programs need to prepare around a common set of disclosure building blocks. These areas show up repeatedly across the ESRS structure and should anchor your design work from the start.

Core Elements required for CSRD reporting

Governance: How the board and management oversee sustainability matters, responsibilities, and decision-making.

Strategy: How sustainability topics influence business model, resilience, priorities, and long-term direction.

Impacts: The organization’s actual or potential effects on people and the environment.

Risks: Sustainability-related factors that could negatively affect performance, assets, operations, or reputation.

Opportunities: Potential business upside linked to sustainability trends, innovation, markets, or efficiency.

Metrics: Quantitative indicators used to measure performance on material sustainability topics.

Targets: Time-bound objectives and benchmarks used to track progress.

Policies: Formal commitments and internal rules that guide action and accountability.

Actions: Programs, investments, remediation measures, and initiatives taken to address material topics.

Value chain coverage: Consideration of upstream suppliers and downstream customers, distributors, and end use.

Transition planning: Plans to adapt the business toward stated sustainability outcomes, often including climate transition considerations.

Value chain considerations are especially important. Many material topics do not sit neatly within the four walls of the company. Procurement practices, product use, logistics, labor conditions, and downstream impacts may all affect what needs to be disclosed. That raises the bar for supplier engagement, data estimation, and governance.

How CSRD connects to finance and annual reporting

CSRD reporting is closely connected to financial reporting, management reporting, and investor communications. Sustainability disclosures are not meant to sit in isolation. They must align with the way the company describes strategy, risk, capital allocation, and performance.

This is why finance plays a central role. Finance teams understand consolidation, controls, close processes, and assurance expectations. They are often best positioned to:

Define reporting calendars

Standardize entity submissions

Validate quantitative metrics

Coordinate review and sign-off

Align sustainability disclosures with annual reporting narratives

When sustainability reporting is disconnected from finance, inconsistencies emerge fast. Risks described in sustainability sections may not align with annual report language. Targets may lack budget linkage. Metrics may lack controls. Mature CSRD reporting programs avoid this by treating sustainability disclosure as part of enterprise reporting, not a separate storytelling exercise.

Double materiality explained step by step

Double materiality is one of the defining features of CSRD reporting, and also one of the most misunderstood. Many teams know the phrase but struggle to operationalize it. The goal is not to run a one-off workshop. The goal is to create a repeatable, documented assessment that explains why certain topics are material and how that conclusion drives disclosure.

What double materiality means

Double materiality requires companies to evaluate sustainability topics through two lenses.

Impact materiality asks: how does the company affect people and the environment?

Financial materiality asks: how do sustainability matters create risks or opportunities that affect the company’s financial position, performance, cash flows, access to finance, or enterprise value over time?

Both lenses are required because the directive is designed to show not only what sustainability means for the company, but also what the company means for society and the environment. A topic can be material under one lens, the other, or both.

A simple example helps:

A company’s emissions may be impact material because they affect climate.

Those same emissions may be financially material if carbon costs, customer pressure, or transition regulation affect profitability.

Workforce safety may be impact material because of harm to employees, and financially material if incidents disrupt operations or create legal exposure.

A practical assessment process

A defensible double materiality process should be structured, evidence-based, and cross-functional. As a consultant, I advise organizations to follow a staged approach rather than trying to solve everything in one workshop.

Step 1: Identify stakeholders and decision-makers

Start by defining who needs to be consulted and who approves outcomes. This usually includes sustainability, finance, legal, risk, HR, procurement, operations, and executive sponsors. Consider external stakeholders where relevant, such as investors, customers, suppliers, workers, or affected communities.

Step 2: Build a topic universe

Create a long list of sustainability matters relevant to your sector, footprint, products, and value chain. Use existing risk registers, policy commitments, customer requirements, peer disclosures, and internal subject matter expertise to avoid blind spots.

Step 3: Map impacts, risks, and opportunities

For each topic, document the actual or potential impacts on people and the environment, along with financial risks and opportunities for the business. Include upstream and downstream value chain effects where material.

Step 4: Define criteria and scoring logic

Set clear criteria for severity, likelihood, scale, scope, remediation difficulty, time horizon, and financial effect. Agree scoring thresholds in advance. This prevents teams from changing the rules halfway through the assessment.

Step 5: Prioritize and validate topics

Use workshops, interviews, and scoring reviews to rank topics. Then validate findings with senior leadership and control functions. Materiality outcomes should be reviewed for consistency with strategy, risk management, and public commitments.

Step 6: Document rationale and link to disclosures

Record why each topic was classified as material or not material. Then map material topics directly to ESRS disclosure requirements, required metrics, and evidence expectations.

The most common failure points in CSRD reporting are process failures, not technical failures.

1. Treating the exercise as a one-time workshop

Materiality must be maintained, not performed once and forgotten. Business model changes, acquisitions, regulatory changes, and stakeholder expectations can all shift materiality conclusions.

2. Ignoring upstream and downstream value chain impacts

Many organizations focus only on owned operations because the data is easier to access. That creates a distorted assessment and can leave major impacts or risks unaddressed.

3. Failing to connect material topics to governance, metrics, and evidence

A topic is not truly embedded just because it appears on a matrix. If there is no owner, no KPI, no policy linkage, and no documentation trail, the disclosure will be weak under assurance.

How to prepare your organization for compliance

The organizations that perform best on CSRD reporting treat it like a transformation program. They do not assign it to one department and hope for the best. They build governance, define workflows, implement controls, and create a phased roadmap.

Build the right operating model

Start with ownership. Sustainability may lead content, but finance should co-own reporting process design. Legal, compliance, HR, procurement, and IT all have defined roles. Executive accountability must also be explicit, especially for approvals and escalation.

Your operating model should include:

A steering committee with executive sponsorship

Entity-level and topic-level owners

Defined review and sign-off cycles

Escalation paths for gaps or judgment calls

Board or committee oversight for material decisions

The strongest programs also define a reporting calendar that aligns with financial close, annual report drafting, and audit planning. This reduces duplication and prevents last-minute disclosure conflicts.

Strengthen data, controls, and assurance readiness

This is where many CSRD reporting efforts become operationally difficult. Teams discover that required data sits in spreadsheets, emails, vendor portals, and local systems with inconsistent definitions. You need a controlled data architecture, even if some workflows remain manual at first.

Focus on three priorities:

Map required data sources, owners, and systems

Create an inventory of each metric and narrative input, including system of record, owner, refresh cycle, and methodology.

Design documentation trails and internal controls

For material disclosures, define evidence requirements, reviewer roles, version control, and approval checkpoints.

Prepare for limited assurance

Assume an independent reviewer will ask how a figure was generated, who approved it, what assumptions were used, and where supporting records are stored.

A practical roadmap should sequence work in the order that reduces downstream rework. In most cases, that means starting with applicability and gap analysis before investing heavily in data collection.

A proven sequence looks like this:

Scoping and applicability assessment

Confirm which entities, reporting boundaries, and timelines apply.

Gap analysis against ESRS

Identify missing disclosures, weak processes, and unclear ownership.

Double materiality assessment

Determine material topics and map them to reporting requirements.

Data model and process design

Build metric definitions, source mappings, controls, and workflows.

Drafting and review

Prepare disclosures, align with annual reporting, and validate narratives.

Assurance preparation and remediation

Test evidence, resolve gaps, and strengthen documentation.

Best practice is to set milestones not only for disclosures, but also for policy updates, training, technology enablement, and board oversight. If those enablers lag, reporting quality will lag too.

4 best practices from the field

1. Appoint joint leadership from sustainability and finance

This prevents a split between narrative ambition and reporting discipline. One team cannot do this alone.

2. Standardize definitions before collecting data

Do not launch enterprise data collection until you define methodologies, boundaries, units, and ownership. Otherwise you create noise, not insight.

3. Run a mock assurance review early

Test a sample of disclosures as if an assurance provider were already reviewing them. This exposes documentation weaknesses before filing pressure peaks.

4. Build dashboards for readiness, not just final reporting

Executives need visibility into scope decisions, data gaps, overdue owners, and control failures long before the report is published.

How is CSRD different from earlier sustainability reporting rules?

CSRD reporting is broader, more standardized, and more rigorous than earlier EU sustainability disclosure rules. It expands the number of companies affected, requires reporting under ESRS, emphasizes double materiality, integrates sustainability information into management reporting, and introduces stronger expectations for digital reporting and assurance readiness. In short, it moves sustainability disclosure closer to the discipline of financial reporting.

How detailed does value chain reporting need to be?

Value chain reporting should be detailed enough to reflect material upstream and downstream impacts, risks, and opportunities. That does not mean perfect visibility across every supplier and customer on day one. It does mean you need a documented approach for identifying material value chain areas, using available data, estimates where appropriate, and clear explanations of methodologies and limitations. The key is reasoned, evidence-based coverage rather than superficial statements.

What should enterprise teams do in the next 90 days?

If your organization is preparing for CSRD reporting, the next 90 days should focus on high-impact groundwork:

Confirm legal scope across all relevant entities

Launch or refresh your ESRS gap assessment

Set up cross-functional governance with executive sponsorship

Design your double materiality methodology and stakeholder plan

Inventory required data sources, owners, and system gaps

Identify disclosures likely to face the greatest assurance risk

These actions create momentum and reduce the chance that your program stalls at the drafting stage.

Build CSRD reporting faster with FineReport

Building this manually is complex; use FineReport to utilize ready-made templates and automate this entire workflow.

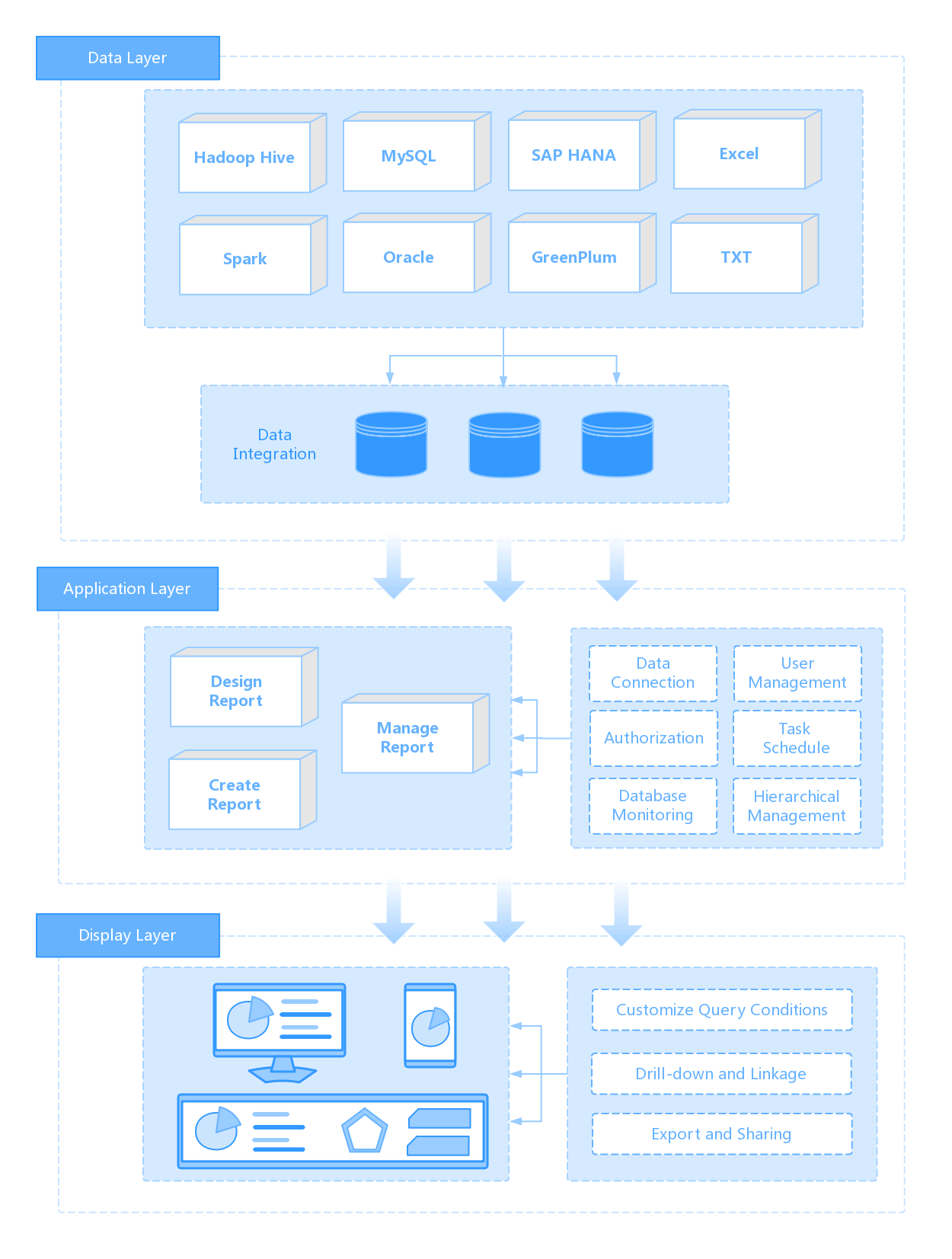

FineReport helps enterprise teams operationalize CSRD reporting with structured dashboards, multi-source data integration, workflow visibility, and audit-friendly reporting processes. Instead of chasing spreadsheets across departments, you can centralize entity scope, ESRS mapping, materiality results, KPI collection, approvals, and readiness tracking in one reporting environment.

That matters because CSRD reporting is not just a disclosure problem. It is a management systems problem. FineReport gives operations leaders, finance teams, and sustainability managers a practical way to monitor progress, standardize submissions, and produce executive-ready reporting dashboards throughout the compliance cycle.

Get Ready-to-Use Dashboard Templates in Fine Gallery

With FineReport, you can support key CSRD reporting use cases such as:

Scope and entity applicability tracking

ESRS disclosure planning and ownership management

Double materiality scoring dashboards

Sustainability KPI consolidation across business units

Evidence and assurance readiness monitoring

Board and executive progress reporting

If your team needs to move from fragmented spreadsheets to a controlled enterprise reporting process, this is the fastest path to execution.

CSRD reporting is the EU sustainability disclosure process that requires companies to report how sustainability issues affect the business and how the business affects people and the environment. It is a regulated, auditable reporting requirement rather than a voluntary ESG narrative.

Companies can be in scope based on factors such as EU listing status, company size, legal structure, and EU revenue or operations. Non-EU groups may also be affected if they have qualifying subsidiaries, branches, or significant business activity in Europe.

ESRS are the European Sustainability Reporting Standards that define what companies need to disclose under CSRD. They matter because they turn broad legal requirements into specific disclosure topics, data points, and reporting expectations.

A double materiality assessment identifies both how sustainability topics create risks or opportunities for the company and how the company impacts society and the environment. It helps determine which topics are material and therefore need to be disclosed.

Companies should document scope decisions, assign disclosure owners, map data sources, and maintain clear evidence trails for reported information. Strong controls, review workflows, and traceable supporting records make assurance much smoother.

Product Trial

FineReport

Pixel-perfect reports · Interactive dashboards · Easy data entry · Digital twins