Public sector financial reporting is not just an accounting exercise. It is how governments, agencies, municipalities, public hospitals, universities, and other public entities show whether public money was used as intended, whether services can be sustained, and where financial risks are building.

For decision-makers, the challenge is rarely a lack of reports. It is turning dense financial statements, budget documents, and operational dashboards into timely, reliable decisions. With FineReport + Dora, teams can ask for a report summary in chat, generate structured narratives from trusted report assets, receive scheduled briefings, and push exceptions to the right owner.

Click To Try The Dashboard

All reports in this article are built with FineReport

What public sector financial reporting is and why it matters

Public sector financial reporting is the structured presentation of a public entity’s financial position, financial performance, cash flows, budget execution, and supporting disclosures. In plain language, it tells stakeholders:

what the entity owns and owes

how resources were raised and used

whether spending matched approved budgets

what financial risks may affect future service delivery

This matters because public entities are accountable for more than profit. They are responsible for stewardship of taxpayer funds, delivery of public services, compliance with laws and budget approvals, and long-term sustainability of programs and infrastructure.

In the private sector, financial reporting is often judged primarily by profitability, return, and shareholder value. In the public sector, the picture is broader. A public entity may run a deficit in a given period and still be performing an important policy function. Equally, a reported surplus does not automatically mean strong performance if infrastructure is deteriorating, grant income is temporary, or services are under-delivered.

That is why senior officials, finance teams, audit committees, oversight bodies, and elected decision-makers rely on public sector financial reporting to answer questions such as:

Are we financially sustainable?

Are we using funds as authorized?

Can we maintain service capacity next year and beyond?

Are liabilities or commitments building up off the main budget narrative?

Where do we need intervention before problems escalate?

This is also where modern reporting operations matter. FineReport provides the trusted reporting foundation for formatted statements, budget comparison reports, management cockpits, and recurring financial packs. Dora adds an enterprise Data Agent layer so leaders do not have to manually interpret every schedule or wait for analysts to explain each variance. Instead, they can consume governed, chat-based summaries and exception follow-up built on trusted report assets.

The 5 core statements decision-makers should understand

Statement of financial position

The statement of financial position shows the entity’s assets, liabilities, and net assets or equity at a point in time. It is the public sector version of a balance sheet.

Report Element: Assets Definition: Resources controlled by the entity, such as cash, receivables, infrastructure, property, equipment, and investments. Business value: Helps leaders understand resource capacity and what supports future services. AI use:Dora can summarize major asset categories, flag rapid changes, and explain whether movements are tied to capital projects, revaluations, or disposals.

Report Element: Liabilities Definition: Present obligations, including payables, borrowings, pension obligations, provisions, and other commitments recognized on the statement. Business value: Reveals debt burden, future cash pressure, and exposure that may limit flexibility. AI use:Dora can identify liability growth, highlight unusual increases, and prepare a management briefing on debt maturity or pension-related pressure points.

Report Element: Net assets or equity Definition: The residual interest after liabilities are deducted from assets. Business value: Indicates the entity’s financial base and resilience over time. AI use:Dora can explain how current-year results, revaluation reserves, or prior-period adjustments affected the closing balance.

For decision-makers, this statement is especially useful for assessing long-term resilience. A healthy service organization can still face structural stress if debt is rising faster than revenue capacity or if key assets require major renewal.

Statement of financial performance

The statement of financial performance shows revenue, expenses, and the resulting surplus or deficit for the reporting period.

Report Element: Revenue Definition: Inflows such as taxes, grants, service fees, transfers, and other funding sources. Business value: Shows how the entity funds operations and whether revenue is stable or dependent on one-off items. AI use:Dora can break down recurring versus non-recurring revenue and include grant concentration insights in a scheduled financial summary.

Report Element: Expenses Definition: Outflows or consumption of resources, including payroll, supplies, depreciation, interest, and program spending. Business value: Helps track cost pressure, efficiency, and whether spending patterns are sustainable. AI use:Dora can explain expense spikes, compare major cost lines to prior periods, and identify departments requiring follow-up.

Report Element: Surplus or deficit Definition: The net result after revenue minus expenses. Business value: Provides a high-level indicator of operating performance, but must be interpreted alongside budget, cash, and service outcomes. AI use:Dora can generate a structured report summary explaining the main drivers of the period result rather than just restating the number.

In the public sector, a surplus or deficit is only part of the story. Decision-makers should ask what caused it, whether it reflects sustainable operations, and whether services were delivered effectively.

Cash flow statement

The cash flow statement shows actual cash inflows and outflows, grouped into operating, investing, and financing activities.

Report Element: Operating cash flows Definition: Cash generated from or used in day-to-day activities. Business value: Indicates whether regular operations are generating enough cash to support services. AI use:Dora can explain why cash from operations differs from the surplus or deficit and flag short-term liquidity risks.

Report Element: Investing cash flows Definition: Cash used for capital expenditure or received from asset sales and investment activity. Business value: Shows how much the entity is spending on infrastructure and future service capacity. AI use:Dora can summarize capital program cash use and connect large movements back to project reports in FineReport.

Report Element: Financing cash flows Definition: Cash flows related to borrowing, debt repayment, and other financing arrangements. Business value: Reveals whether the entity is relying more heavily on debt or other financing sources. AI use:Dora can generate an exception note when financing needs rise unexpectedly or when debt service pressure increases.

Cash matters because even entities with a strong accrual-based result can face operational stress if cash collections are delayed, grants arrive late, or capital payments spike.

This statement explains how the entity’s net assets or equity changed during the reporting period.

Report Element: Accumulated surpluses or deficits Definition: The cumulative effect of prior and current operating results. Business value: Shows whether the entity is building or eroding its financial base over time. AI use:Dora can produce a period-over-period explanation of how the accumulated position changed.

Report Element: Revaluations and reserve movements Definition: Adjustments related to valuation changes or specific reserves. Business value: Helps distinguish operating performance from valuation-driven changes. AI use:Dora can separate operating impacts from revaluation impacts in a chart-based answer.

Report Element: Other adjustments Definition: Items such as corrections, transfers, or policy-related movements. Business value: Important for understanding whether reported changes come from performance, accounting changes, or special events. AI use:Dora can highlight unusual entries that deserve board or audit committee review.

This statement is useful because it prevents decision-makers from assuming that all changes in financial strength come from annual operations alone.

Budget comparison and notes to the financial statements

Budget comparison reporting and the notes are essential for interpretation. In many public entities, these sections are where the most decision-relevant context appears.

Report Element: Budget-to-actual comparison Definition: A view of approved budget figures compared with actual outcomes. Business value: Shows whether resources were used as authorized and where execution issues occurred. AI use:Dora can automatically summarize material variances, assign owners, and prepare variance briefings before review meetings.

Report Element: Accounting policies and estimates Definition: The rules, judgments, and assumptions used in preparing the statements. Business value: Explains how numbers were produced and whether comparability may be affected. AI use:Dora can surface note disclosures that may materially affect interpretation when users ask about sudden changes.

Report Element: Commitments and contingencies Definition: Future obligations or possible liabilities not fully reflected in current balances. Business value: Helps detect hidden exposure and future fiscal pressure. AI use:Dora can flag contingency-related disclosures in scheduled risk briefings.

Report Element: Program and operational context Definition: Narrative explanations that connect financial results to service delivery, policy shifts, and implementation conditions. Business value: Prevents narrow interpretation of financial data without operational reality. AI use:Dora can combine report figures with approved commentary templates to produce more useful management narratives.

IPSAS concepts that make the statements easier to read

The role of the IPSAS conceptual framework

The IPSAS conceptual framework helps public sector entities prepare general purpose financial reports that are useful for accountability and decision-making. Its role is to guide how standards are developed and how financial information should be recognized, measured, presented, and disclosed when specific issues arise.

For decision-makers, the practical benefit is consistency. The framework reflects the fact that public sector entities exist mainly to deliver services, not simply to generate profits. That means the reporting model must support assessment of both financial health and service capacity.

A useful way to think about the framework is that it gives structure to four core questions:

In an enterprise reporting environment, FineReport can standardize how these framework-based reporting outputs are presented across departments and entities. Dora then helps users consume them more effectively through governed summaries and question-answering tied to approved definitions and templates.

Qualitative characteristics of useful information

Good public sector financial reporting is not only technically compliant. It also needs to be useful. That is where the qualitative characteristics matter.

Relevance: Information should help users make decisions or assess accountability.

In practice, material variances, debt trends, and major commitments are relevant because they affect future options.

Faithful representation: Information should reflect the underlying economic reality as accurately as possible.

This matters when recognizing liabilities, estimating provisions, or reporting grant conditions.

Understandability: Reports should be clear enough for informed non-specialists to follow.

Good notes, structured summaries, and variance explanations improve understandability.

Timeliness: Information should arrive soon enough to support action.

A perfect report that arrives too late has limited value for policy or budget control.

Comparability: Users should be able to compare periods, programs, and entities on a consistent basis.

This requires stable policies and clear disclosure of changes.

Verifiability: Information should be capable of being checked and supported.

This strengthens auditability and trust.

These characteristics are a strong reason to adopt AI carefully. Dora is useful because it works as an enterprise Data Agent over governed reporting assets, not as an unguided text generator. FineReport provides the trusted statements, metrics, templates, and permission structure. Dora helps convert those assets into understandable, timely, and repeatable briefings.

One of the main reasons public sector statements can be hard to interpret is that different accounting bases and measurement approaches can tell different stories.

Cash basis vs accrual basis

Cash basis reporting records transactions when cash is received or paid.

Accrual basis reporting records revenue and expenses when they are earned or incurred, regardless of when cash moves.

Cash basis is simpler and highlights immediate liquidity. Accrual basis provides a fuller picture of obligations, asset use, and long-term sustainability. Decision-makers should know which basis is being used, because a healthy cash position does not necessarily mean strong long-term finances, and a deficit on an accrual basis does not necessarily mean short-term cash distress.

Historical cost, fair value, and other measurements

Measurement choices can also change the story.

Historical cost emphasizes original transaction values.

Fair value reflects current market-based estimates where appropriate.

Other measurement approaches may be used depending on the asset or liability.

For example, infrastructure, investments, or specialized assets may look different depending on valuation methods. Pension obligations and provisions may also change materially based on assumptions.

That is why decision-makers should never read top-line figures without the related notes. A change in measurement basis, valuation assumptions, or policy application can reshape trend analysis.

What decision-makers should actually monitor in public sector reports

Financial sustainability and service capacity

Many leaders make the mistake of focusing first on the annual surplus or deficit. A better starting point is whether the entity can maintain service delivery over time.

Key areas to monitor include:

liquidity and short-term cash sufficiency

debt levels and debt servicing burden

asset condition and infrastructure replacement needs

growth in unfunded obligations

the capacity to sustain mandated services without emergency funding

In a FineReport management cockpit, these indicators can be tracked together instead of in isolated documents. Dora can then turn the cockpit into a recurring executive briefing by summarizing threshold breaches, trend changes, and owner actions.

Budget execution is central in the public sector because authorization and accountability matter as much as the final accounting result.

Decision-makers should watch for:

significant overspending or underspending

recurring variance in the same departments or programs

delays in capital project execution

funding gaps caused by lower-than-expected revenue

spending patterns that differ from approved policy intent

Underspending is not always positive. It can indicate implementation delays, staffing shortages, procurement bottlenecks, or inability to deliver planned services. Overspending may point to weak control, demand pressure, or underestimated costs.

A governance-ready reporting workflow should not stop at showing the variance. It should also support explanation, alerting, and follow-up. This is where FineReport + Dora becomes practical rather than theoretical.

Revenue quality, expense pressures, and balance sheet exposures

Some of the most important risks in public sector financial reporting are hidden in revenue composition, expense trends, and balance sheet details.

Decision-makers should monitor:

reliance on one-off revenues

heavy dependency on grants or transfers

payroll growth outpacing funding growth

pension and employee benefit obligations

guarantees, legal claims, and other exposure

rising receivables or doubtful collection patterns

These issues affect future flexibility. A government entity may appear stable today while quietly becoming more exposed to external funding shifts, labor cost escalation, or long-tail liabilities.

For finance leaders, the most useful question is often not “What is the current result?” but “What is reducing our room to maneuver next year?”

Disclosures, assumptions, and audit signals

The notes and audit-related signals often change the meaning of the core statements.

Decision-makers should pay attention to:

significant accounting judgments

estimation uncertainty

contingent liabilities

going-concern or sustainability-related concerns where relevant

emphasis matters and recurring audit findings

changes in accounting policy or presentation

scope changes due to restructurings, consolidations, or program transfers

A clean top-line view can still hide important uncertainty if disclosures reveal material assumptions or unresolved control weaknesses. That is why financial reporting should be consumed together with note analysis, audit commentary, and budget context.

Public sector finance teams already produce statements, board packs, budget variance reports, and audit committee materials. The bottleneck is often report consumption: reviewing large packs, identifying what changed, summarizing what matters, and following up with the right owners.

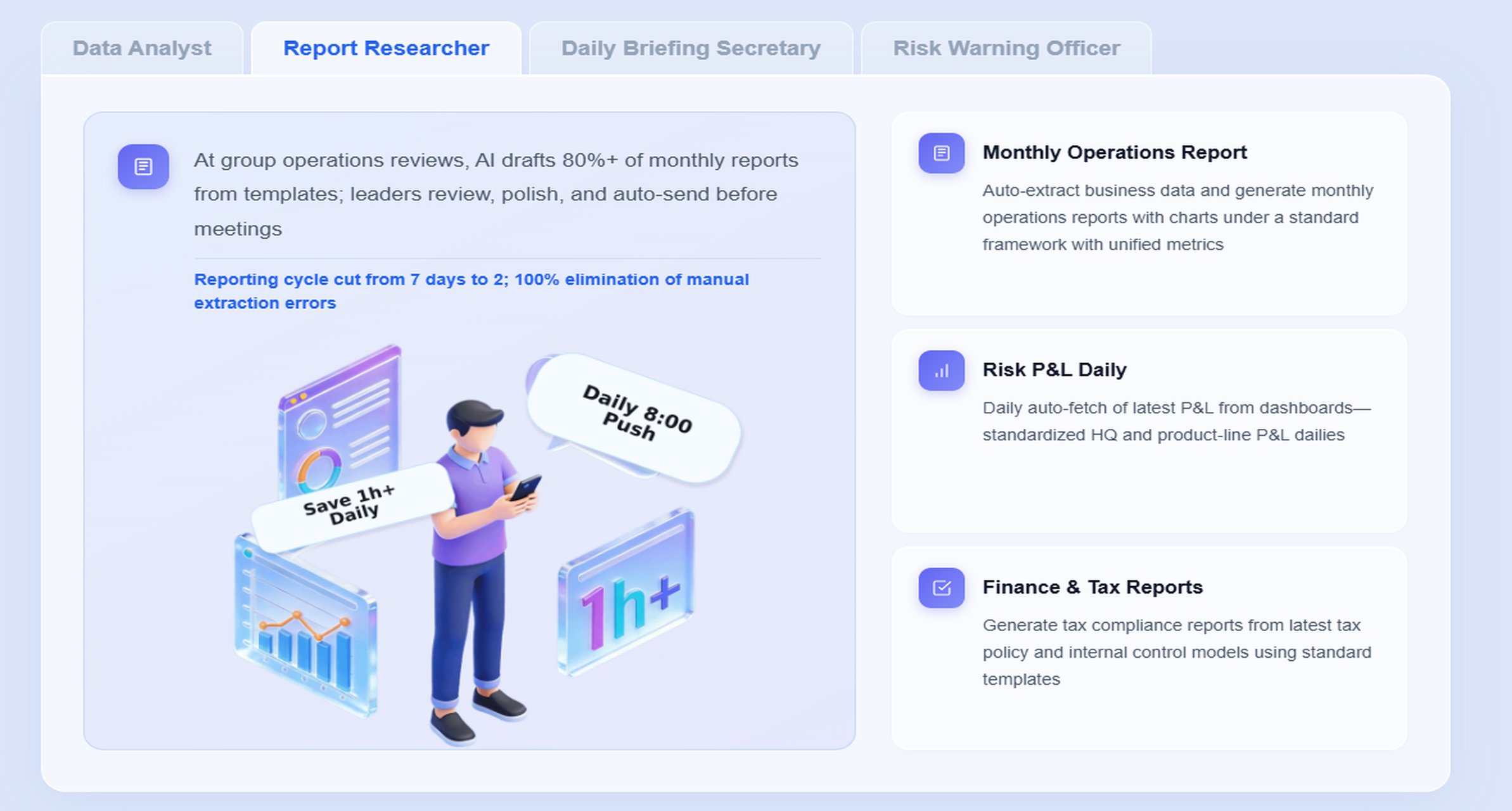

Dora addresses this as an enterprise Data Agent layered on top of FineReport and existing trusted reporting assets. For this scenario, the most relevant digital employee is the Daily Briefing Secretary, supported by Risk Alert Officer capabilities for variance and exposure monitoring.

Scenario-specific chat example:

“Summarize this quarter’s public sector financial reporting pack, highlight material budget variances, identify any liquidity or liability risks, and list the departments that need follow-up.”

Retrieve trusted FineReport report or operational cockpit data. Dora pulls the approved statement pack, budget comparison report, and financial risk cockpit from FineReport.

Understand KPI definitions, templates, filters, and business terms. Dora uses the governed semantic layer, approved metric definitions, budget mappings, and reporting templates established in FineReport.

Generate a structured report summary in chat. Dora produces a management-ready narrative covering statement movements, cash position, major variances, and notable disclosures.

Detect exceptions and execution risks. Dora highlights threshold breaches such as overspending, delayed capital execution, rising liabilities, or weakening operating cash flow.

Push insights to the right owners.

The Daily Briefing Secretary sends scheduled summaries to finance leadership, while the Risk Alert Officer routes exceptions to department heads or budget owners.

Create follow-up records and recurring briefings. Dora logs action items, prepares daily or weekly summaries, and supports periodic review meetings with updated status.

This matters because public sector reporting is highly repetitive but also highly sensitive to governance. Leaders need speed, but they also need controlled outputs. FineReport provides the trusted reporting and semantic foundation: formatted statements, cockpit views, budget reports, note-linked schedules, permissions, and KPI governance. Dora improves execution through:

natural-language query over trusted reporting assets

chat-based AI assistant for report consumption

chart explanations and structured report summaries

scheduled daily, weekly, monthly, or quarterly briefings

exception alerts and owner push notifications

follow-up support for recurring financial review workflows

This is also where Dora differs from prompt-only tools. Public sector financial reporting requires permissions, controlled terminology, approved templates, and auditable workflow behavior. Dora’s skills-based execution is designed for more stable and controllable enterprise use, with better landing capability than feature-only agent comparisons. Instead of treating every request as a blank-prompt exercise, Dora can work through governed AI workflows tied to real reporting assets.

For executives, this means faster access to actionable summaries. For IT and data teams, it means they shift from manually answering every report question to maintaining trusted connections, semantic rules, templates, and reusable Skills. For finance users, it means timely answers without hunting through dense packs or waiting for ad hoc interpretation.

How to interpret public sector financial statements with more confidence

A practical reading order for non-specialists

If you are not a technical accountant, a good reading order can improve your judgment quickly.

Start with the audit opinion and any highlighted matters.

Review the statement of financial position for resilience and exposure.

Read the statement of financial performance for operating trends.

Check the cash flow statement for liquidity reality.

Review the statement of changes in net assets or equity for the bigger movement story.

Examine budget-to-actual variances.

Read the major notes, especially policies, estimates, contingencies, and commitments.

Connect the financial statements to service delivery and operational performance reports.

This sequence helps you avoid being overly influenced by a single headline number.

Questions to ask when comparing entities or periods

Comparisons are useful only when the underlying basis is understood. Ask:

Were the same accounting policies used?

Did the scope of the entity change?

Were there unusual transactions or one-off grants?

Did inflation or revaluation materially affect comparability?

Did capital spending rise because of expansion, catch-up maintenance, or emergency response?

Did improved financial results also improve service delivery?

Are year-over-year changes due to genuine performance or classification changes?

A strong reporting process should make these questions easier to answer. FineReport can standardize comparison templates across periods and organizations, while Dora can surface policy changes or unusual items when users ask for variance explanations in chat.

Common mistakes to avoid

Several mistakes repeatedly weaken interpretation:

focusing only on surplus or deficit

ignoring cash constraints

overlooking note disclosures

treating underspending as automatically positive

comparing figures without considering policy or scope changes

assuming strong revenue today means sustainable revenue tomorrow

missing off-balance-sheet or contingency-related warning signs

Good public sector financial reporting requires context, not just numbers. That is why summary, explanation, and follow-up matter as much as statement production.

Helpful reference points and illustrative examples

Decision-makers who want to go deeper should look at recognized global standard-setting and guidance materials related to public sector reporting, especially IPSAS-oriented conceptual guidance, illustrative financial statements, and audit office examples. These help readers see how high-quality public sector financial reporting is structured in practice.

Useful learning approaches include:

reviewing IPSAS-oriented explanatory materials to understand recognition, measurement, presentation, and disclosure concepts

studying illustrative public sector financial statements to see how notes and core statements work together

examining audit office examples to understand common weaknesses and better-practice presentation

comparing financial statements with budgets, performance reports, and audit commentary for a fuller accountability picture

In practice, the best understanding comes from connecting three layers:

That combined view is exactly where a modern reporting foundation becomes valuable. FineReport can assemble these layers into a governed reporting environment, and Dora can help decision-makers consume them in a more usable way through structured summaries, recurring briefings, and exception-based follow-up.

1. Standardize report templates, KPI definitions, and business terms

Public sector financial reporting becomes easier to interpret when core statements, variance reports, and management packs follow a consistent structure. Standard definitions for terms like operating surplus, capital commitment, grant dependency, and liquidity pressure reduce confusion across departments.

This also improves AI readiness. Dora performs best when it can rely on approved templates, KPI definitions, and business language rather than inconsistent local formats.

2. Build a semantic layer inside the reporting workflow

Do not treat reporting logic as scattered spreadsheet knowledge. Centralize metric definitions, mappings, filter rules, and approved dimensions in the reporting environment.

FineReport serves as the trusted reporting foundation here. Dora then uses that semantic layer to deliver governed answers, structured report summaries, and chart-based explanations instead of ungrounded text responses.

3. Treat data quality as part of the AI implementation

AI does not fix weak source data, unclear reconciliations, or inconsistent classifications. Before expanding automation, validate critical balances, budget mappings, organizational hierarchies, and disclosure inputs.

The more trusted the FineReport reporting assets are, the more reliable Dora’s briefings, summaries, alerts, and follow-up outputs will be.

4. Start with high-value recurring reports

Do not try to automate every financial report at once. Begin with recurring, time-sensitive, high-friction use cases such as:

monthly finance leadership packs

quarterly budget variance reviews

audit committee briefing summaries

cash and liability monitoring reports

department-level exception follow-up

This creates faster adoption and clearer governance.

5. Define alert thresholds, ownership rules, and review controls

AI-driven report consumption works best when exception rules are explicit. Set thresholds for overspending, delayed execution, liability changes, cash deterioration, or note-triggered risk items. Also define who receives alerts, who reviews AI-generated narratives, and when escalation is required.

This protects governance while allowing Dora to function as a practical AI digital employee for repeatable reporting workflows.

Building this manually is complex. FineReport helps teams standardize trusted reports, operational cockpits, templates, and reporting workflows. Dora turns those assets into an AI assistant that can answer report questions in chat, generate structured summaries, push scheduled briefings, monitor exceptions, and follow up with responsible owners.

For public sector financial reporting, this means an organization can move beyond static statement distribution toward a more actionable reporting process:

finance teams publish trusted core statements and budget comparison reports in FineReport

leaders review operational cockpits for liquidity, liabilities, variances, and service-related indicators

Dora acts as a Daily Briefing Secretary, Report Researcher, Data Analystdigital employee, or Risk Alert Officer depending on the workflow

departments receive timely summaries, exceptions, and follow-up prompts without breaking governance boundaries

FineReport + Dora is not only a reporting upgrade; it is a practical fourth-generation Agentic BI path.FineReport provides governed reports and operational cockpits. Dora provides the AI assistant layer for scenario execution, with more controlled Skills, lower token waste, faster execution paths, and more stable workflows than prompt-only agents.

Get Ready-to-Use Dashboard Templates in Fine Gallery

The strongest Dora pitch is scenario + product + service: FineReport provides the trusted reporting foundation, Dora provides the AI digital employee, and implementation service connects data, governance, semantic setup, Skills, report templates, permissions, and rollout.

For public entities that need better transparency, faster interpretation, and more reliable follow-up, that is the practical path forward.

The core statements usually include the statement of financial position, statement of financial performance, statement of cash flows, statement of changes in net assets or equity, and budget comparison information with supporting notes. Together, they show financial health, operating results, liquidity, and budget execution.

Public sector reporting focuses on accountability, service delivery, budget compliance, and long-term sustainability rather than profit alone. A surplus or deficit matters, but decision-makers also need to understand whether public funds were used as authorized and whether services can be maintained.

IPSAS refers to international accounting standards designed for public sector entities. It matters because it improves consistency, transparency, and comparability across governments and public organizations.

They should monitor budget variances, cash flow pressure, rising liabilities, asset condition, and reliance on one-off revenue. These signals help identify financial stress before it affects service delivery.

Budget comparison shows whether spending and revenue tracked against approved plans. It helps leaders spot overspending, underdelivery, and areas where corrective action may be needed quickly.

Product Trial

FineReport

Pixel-perfect reports · Interactive dashboards · Easy data entry · Digital twins