Financial reporting rules are not just an accounting issue. For enterprise teams, they shape how transactions are recognized, how disclosures are prepared, how filings are submitted, and how internal controls support the final numbers. In practice, finance leaders must connect external compliance requirements with internal management reporting, review workflows, and evidence retention.

This becomes even more important when reporting is distributed across subsidiaries, regions, ERP systems, and functional owners. A close process can be technically complete yet still produce reporting risk if definitions, review checkpoints, and disclosure support are inconsistent. With FineReport + Dora, teams can ask for a report summary in chat, generate structured narratives from trusted report assets, receive scheduled briefings, and push exceptions to the right owner.

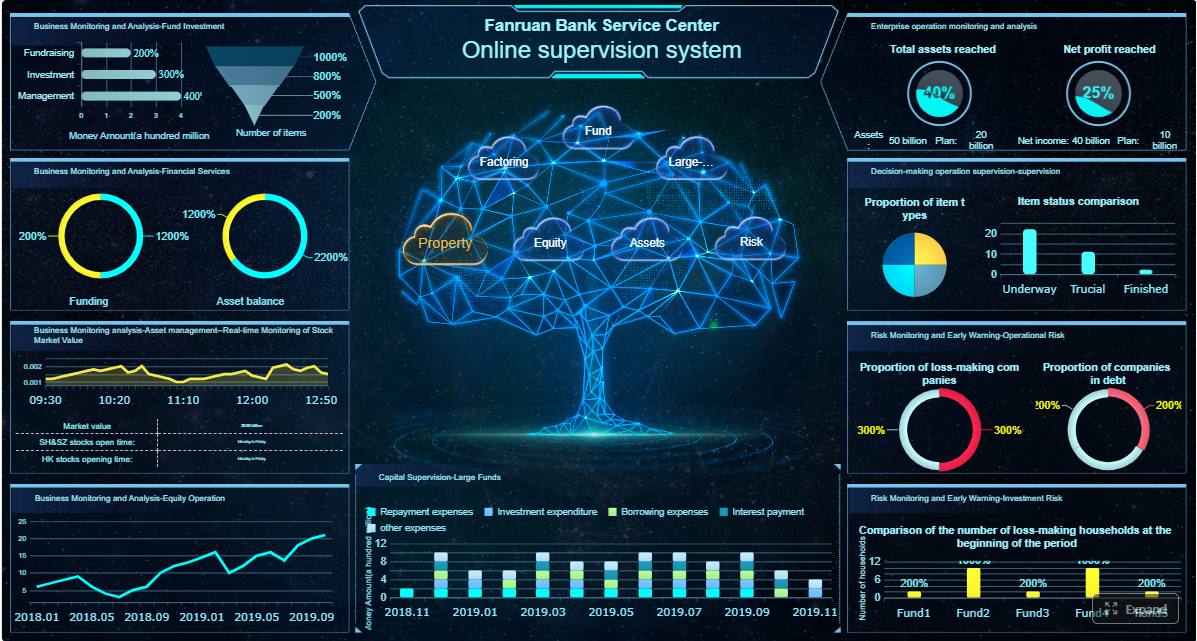

Click To Try The Dashboard

All reports in this article are built with FineReport

Disclosure in notes, management discussion materials, and supporting schedules

Filing and submission requirements for regulated entities

Internal control and documentation expectations that support reliable reporting

For enterprise finance teams, the challenge is that these rules do not come from one single source.

Three layers of financial reporting rules in practice

Regulatory rules

These come from bodies such as the SEC for public-company reporting.

They govern filing obligations, form requirements, deadlines, and certain disclosure expectations.

Accounting standards

These come from frameworks such as US GAAP or IFRS.

They define how transactions should be accounted for and presented.

Internal governance policies

These are company-specific policies, accounting manuals, close calendars, approval workflows, and evidence standards.

They translate external rules into repeatable internal practice.

Enterprise teams need all three layers aligned. A technically correct accounting treatment can still create risk if internal support is weak. Likewise, a strong internal close process can still fail if regulatory disclosures are incomplete or filing instructions are misunderstood.

Why alignment matters beyond compliance

External reporting and internal management reporting often run in parallel, but they should not operate as separate worlds. If the CFO pack, statutory report support, account reconciliations, and SEC filing schedules all use different definitions, finance teams spend more time reconciling reporting outputs than analyzing business performance.

This is where a governed reporting foundation matters. FineReport helps standardize formatted reports, management reports, operational cockpits, recurring close dashboards, and reporting workflows. Dora then acts as an enterprise Data Agent on top of those trusted assets so users can retrieve, summarize, explain, and follow up on reporting outputs in a controlled way.

SEC reporting requirements for public-company finance teams

For public-company finance teams, SEC oversight adds a regulatory layer beyond accounting standards. Finance cannot assume that compliance with GAAP alone satisfies all reporting obligations. SEC requirements affect filing formats, timing, content, and interpretive expectations.

When SEC oversight applies

SEC oversight generally applies when an entity or transaction falls within US securities reporting requirements. In practice, triggers often include:

companies with securities registered in the United States

public offerings and registration statements

periodic reporting obligations for public issuers

significant acquisitions or disposals requiring additional financial disclosures

debt or equity issuance events

material events requiring current reporting

Enterprise reporting teams need to understand not only whether a filing is required, but also which form, which financial statements, which comparative periods, and which disclosures apply.

Common filing areas include:

Annual reports

Quarterly reports

Current event filings

Registration statements

Proxy-related disclosures

Acquisition-related and pro forma financial disclosures

The practical burden is cross-functional. Finance, legal, investor relations, external reporting, tax, treasury, and systems teams often all contribute to one reporting package.

How the SEC Financial Reporting Manual supports compliance

The SEC Financial Reporting Manual is often used by teams as an interpretive aid for presentation and disclosure questions. It helps teams think through issues such as:

However, enterprise teams should distinguish clearly between:

regulatory filing instructions

authoritative accounting standards

internal accounting policy and governance

That distinction matters. A filing instruction may tell the team how or when to present something in a filing, while GAAP determines how the underlying accounting should be recognized and measured. Internal policy then determines how the company documents judgments, review steps, and approval authority.

Digital filing and XBRL reporting expectations

Modern financial reporting also includes structured filing expectations, especially through XBRL tagging. This is no longer a side process handled at the end by one technical specialist. It requires coordination across:

outsourced filing or tagging partners, where applicable

XBRL reporting increases the need for consistency between the financial statements, disclosures, metadata, and system outputs. If line-item definitions or hierarchy relationships are unstable, filing quality suffers.

Key SEC-related report elements enterprise teams should monitor

Filing calendar and due-status dashboard

Definition: A view of upcoming filing dates, draft milestones, review checkpoints, and submission readiness.

Business value: Helps finance and legal teams manage regulatory deadlines and escalation points.

AI use:Dora can summarize pending deadlines, identify overdue review tasks, and push a scheduled filing-readiness briefing.

Disclosure support tracker

Definition: A report showing which note disclosures, support schedules, and approval packages are complete, pending, or under review.

Business value: Reduces last-minute disclosure gaps and improves accountability.

AI use:Dora can generate a structured summary of incomplete disclosures and notify responsible owners.

XBRL tagging exception list

Definition: A report of tagging gaps, mapping issues, or unresolved validation items before filing.

Business value: Improves submission quality and reduces rework near deadline.

AI use:Dora can explain exception patterns and prepare a chart-based answer for filing managers.

GAAP vs IFRS: the main differences enterprise teams must manage

For multinational enterprises, one of the biggest practical issues in financial reporting rules is handling the differences between GAAP and IFRS. Even when the underlying economics are similar, the accounting treatment, presentation, or disclosure outcome can differ enough to require reconciliation and governance.

Core areas where GAAP and IFRS can diverge

Enterprise teams often need special attention in the following areas:

Revenue recognition

Definition: The rules that determine when and how revenue is recognized.

Business value: Revenue is often a key performance measure, investor focus area, and audit priority.

AI use:Dora can summarize revenue trends from trusted reports, explain unusual changes, and flag entities with policy exceptions.

Even where convergence exists, differences can remain in application, industry interpretation, documentation, and disclosure practice.

Leases

Definition: Rules for identifying lease arrangements and recognizing lease-related assets and liabilities.

Business value: Leases affect EBITDA-related analysis, leverage metrics, and disclosure complexity.

AI use:Dora can retrieve lease reporting packs, summarize movement by business unit, and highlight entities with missing review evidence.

Impairment

Definition: The framework used to assess whether assets or cash-generating units have declined in value.

Business value: Impairment judgments are highly sensitive and often require significant management review.

AI use:Dora can compile impairment indicator reports, summarize exception items, and push follow-up tasks to responsible finance owners.

Consolidation

Definition: The rules for determining when an entity should be consolidated, deconsolidated, or equity accounted.

AI use:Dora can provide a structured report summary of ownership changes, entities under review, and pending technical judgments.

Presentation and disclosure

Definition: The way financial information is organized across primary statements and notes.

Business value: Presentation affects transparency, comparability, and regulatory readiness.

AI use:Dora can compare recurring reporting outputs to prior templates and identify sections that need management commentary.

Why reconciliation processes matter

Multinational groups may report under one primary framework while tracking local statutory requirements or internal management measures under another. That creates a need for:

reconciliation logic between local and group reporting

accounting policy governance by topic

standard templates for recurring judgments

threshold-based escalation for complex transactions

review evidence across regions and entities

Without that structure, the group relies too heavily on manual expertise in a small number of people. That creates key-person risk and slows close and reporting cycles.

How to build accounting policies across multiple frameworks

A practical enterprise policy model should define:

the applicable accounting framework by entity and purpose

policy choices and required judgments

materiality thresholds

review and approval authority

documentation expectations

escalation paths for unusual transactions

update procedures when standards change

Consistency matters across business units, regions, and reporting periods. A policy that exists only in a static PDF is not enough. Teams need to operationalize it in recurring reports, review checklists, close controls, and issue logs.

Internal reporting controls that support accurate financial statements

Financial reporting rules are only as strong as the operating controls that support them. Enterprises do not produce reliable statements by policy alone. They need process design, approvals, reconciliations, documentation, and monitoring.

The role of process design, approvals, and documentation

Good internal reporting control starts with process clarity. Teams should know:

who prepares each reporting package

who reviews it

what evidence must be retained

which thresholds trigger escalation

what the due dates are

how unresolved issues are tracked

Core control activities typically include:

Close-process status monitoring

Definition: Tracking completion of close tasks, dependencies, and unresolved issues across entities and functions.

Business value: Reduces bottlenecks and improves reporting timeliness.

AI use:Dora can provide a daily close-status briefing and identify tasks that threaten reporting readiness.

Account reconciliation controls

Definition: Procedures to reconcile ledger balances to subledgers, supporting schedules, and external evidence.

Business value: Reduces balance-sheet risk and supports audit readiness.

AI use:Dora can summarize unreconciled accounts, overdue reconciliations, and high-risk balances for management review.

Review-control evidence tracking

Definition: Confirmation that approvals, commentary, and supporting documents are completed and retained.

Business value: Strengthens governance and supports internal and external audit review.

AI use:Dora can monitor missing review evidence and push follow-up notifications to the control owner.

Role clarity is critical. When responsibilities are unclear, review controls become ceremonial rather than effective. Evidence retention is equally important because a control that cannot be demonstrated may not be considered reliable in an audit or remediation context.

Linking internal controls to external reporting quality

Strong internal reporting controls improve more than close discipline. They directly support:

more reliable disclosures

fewer avoidable filing errors

better management review quality

reduced restatement risk

stronger audit readiness

clearer governance accountability

This linkage is especially important for public companies and large private groups preparing lender, board, or investor reporting. Internal audit, compliance, controllership, and finance operations should work together on:

control testing

issue remediation

recurring exception analysis

policy adherence monitoring

periodic reporting redesign

A trusted reporting environment also creates the conditions for enterprise AI adoption. Dora works best when it sits on top of governed reports, defined KPIs, permission rules, and stable reporting templates built in FineReport.

Financial reporting teams already have reports, reconciliations, close trackers, disclosure checklists, and filing dashboards. The problem is often not report creation alone. It is report consumption: too many files, too many updates, too much manual chasing, and too little time to turn reporting outputs into timely action.

This is where Dora functions as an enterprise Data Agent rather than a generic chat tool. For this scenario, the most relevant digital employees are:

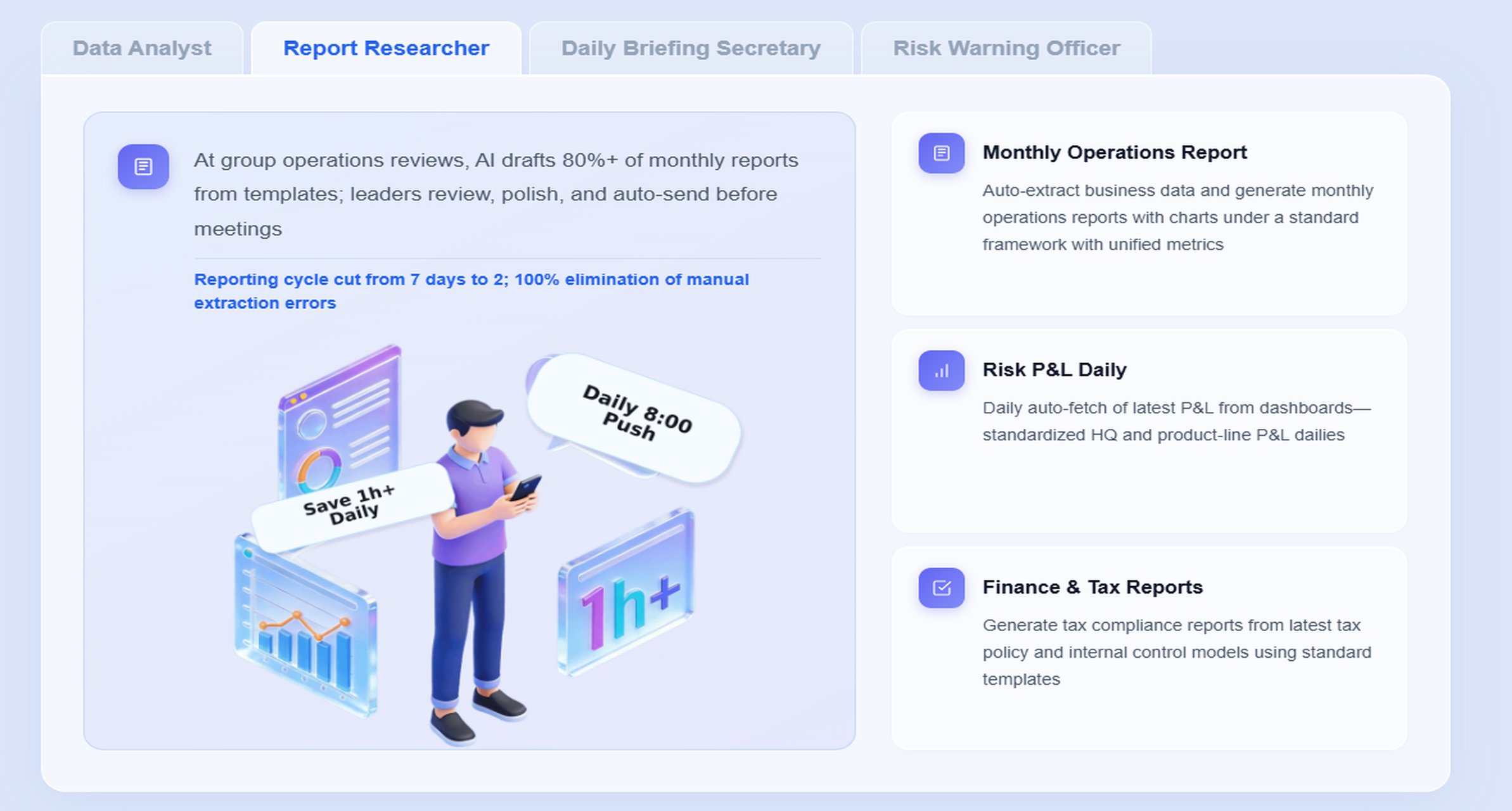

Daily Briefing Secretary for scheduled reporting summaries

Report Researcher for structured report generation from trusted outputs

Risk Alert Officer for exception monitoring and owner notification

“Summarize this quarter’s financial reporting status, highlight overdue reconciliations, list unresolved disclosure support items for the 10-Q package, and show which subsidiaries still have IFRS-to-GAAP adjustment exceptions.”

Instead of manually opening multiple trackers, Dora can work across trusted report assets and return a structured answer linked back to FineReport outputs.

A practical 6-step AI workflow

Retrieve trusted FineReport report or operational cockpit data Dora accesses approved close dashboards, disclosure trackers, reconciliation reports, and policy-based exception lists built in FineReport.

Understand KPI definitions, report templates, filters, business terms, and semantic rules Dora uses the governed semantic layer, including what counts as “overdue,” “unreconciled,” “filing-ready,” or “pending review.”

Generate a structured report summary through chat

It produces a management-ready narrative with counts, trends, exceptions, and links to underlying reports.

Detect exceptions and threshold breaches Dora identifies overdue close items, unresolved XBRL issues, material policy exceptions, or missing review evidence based on predefined rules.

Push summaries, alerts, and suggested follow-up actions

The responsible owner receives a scheduled briefing or exception push instead of waiting for a manual email round-up.

Produce follow-up records for review Dora supports recurring governance by helping maintain action lists, daily summaries, and periodic review records.

Why FineReport matters in this workflow

Dora is effective because FineReport provides the trusted foundation:

operational cockpits for close and filing readiness

reporting workflows for recurring updates

governed permissions and report access boundaries

KPI definitions and business term standardization

Without that foundation, AI outputs can become inconsistent or hard to audit. With FineReport in place, Dora can deliver chat-based AI assistant value in a way that fits enterprise reporting requirements.

Where Dora improves execution

For finance teams, Dora helps move from “people manually preparing and explaining every report” to “AI helping people query, summarize, report, push, alert, and follow up.” In this scenario, the value shows up in several ways:

Natural-language query over trusted reporting assets

Chat-based answers on close, disclosure, and filing status

Structured report summaries and management narratives

Scheduled daily or weekly reporting briefings

Exception alerts for overdue reconciliations or unresolved support

Follow-up prompts to responsible owners

Skills-based execution for more controllable and auditable workflows

This matters because enterprise reporting work is repetitive, deadline-driven, and governance-sensitive. Dora’s governed AI workflow is better suited to this environment than raw prompt-only agents. It is designed for stronger enterprise fit through permissions, semantic rules, KPI governance, report templates, and data quality controls. It also supports more stable execution paths and better landing capability than feature-only agent comparisons.

How enterprise teams create a practical reporting rulebook

A practical reporting rulebook turns scattered requirements into a usable decision framework. It should not be a pile of policy memos stored in shared folders. It should work as an operating model for recurring decisions.

Building a reporting framework for recurring decisions

A useful enterprise rulebook should organize three categories together:

Regulatory guidance

Accounting standards

Company policies and controls

The framework should answer common reporting questions such as:

Which framework applies to this entity and report?

What is the required treatment?

What judgment areas require escalation?

What disclosure support is required?

Who must review and approve the conclusion?

What evidence must be retained?

High-risk topics should be prioritized first, such as:

revenue judgments

consolidation changes

impairment indicators

lease modifications

acquisition accounting

debt and equity classification

non-GAAP or management metric governance

filing-readiness dependencies

Training, updates, and continuous monitoring

A reporting rulebook is only useful if teams keep it current. Enterprises should establish a regular process for:

reviewing standard-setter updates

assessing regulator guidance changes

updating company accounting policies

retraining finance and controllership teams

testing key controls

reviewing recurring exception patterns

strengthening cross-functional communication between finance, legal, compliance, and IT

This is also where reporting technology helps. FineReport can centralize policy-linked reporting views, review dashboards, issue logs, and approval workflows. Dora can then act as a Daily Briefing Secretary or Report Researcher to surface what changed, what is overdue, and what needs management attention.

1. Standardize report templates, KPI definitions, and business terms

If “close complete,” “reconciliation overdue,” or “filing ready” mean different things across teams, reporting quality will drift. Standard definitions improve review consistency and make AI summaries far more reliable.

2. Build a semantic layer inside the reporting workflow

AI adoption fails when reports have inconsistent labels, unclear ownership, or unstable filtering logic. A governed semantic layer helps Dora interpret metrics, thresholds, and business terms correctly across recurring reporting scenarios.

3. Start with high-value recurring reports

Do not try to automate every financial report at once. Focus first on recurring, deadline-driven scenarios such as close-status briefings, disclosure support tracking, reconciliation exception summaries, and filing-readiness reviews.

4. Preserve permissions and approval governance

AI outputs should respect the same access rules as the underlying reports. FineReport provides the reporting and permission foundation, and Dora should operate within those boundaries so summaries and alerts reach the right users only.

5. Use human review for AI-generated report narratives

A structured report summary can save time, but finance leaders should still review narrative outputs, especially for external reporting, sensitive disclosures, or material exceptions. Expand Dora Skills gradually as data quality, templates, and governance mature.

Building this manually is complex. FineReport helps teams standardize trusted reports, operational cockpits, templates, and reporting workflows. Dora turns those assets into an AI assistant that can answer report questions in chat, generate structured summaries, push scheduled briefings, monitor exceptions, and follow up with responsible owners.

For enterprise finance teams dealing with financial reporting rules, this matters because the challenge is not only producing statements. It is also coordinating recurring reporting work across close tasks, accounting policies, control evidence, disclosure support, filing readiness, and management communication.

FineReport can support the reporting foundation through:

formatted financial and disclosure support reports

natural-language query over trusted reporting assets

chart-based answers and structured report summaries

scheduled daily or weekly briefings

exception alerts and push notifications

digital employees for repeatable reporting workflows

controlled Skill execution for auditable enterprise scenarios

FineReport + Dora is not only a reporting upgrade; it is a practical fourth-generation Agentic BI path.FineReport provides governed reports and operational cockpits. Dora provides the AI assistant layer for scenario execution, with more controlled Skills, lower token waste, faster execution paths, and more stable workflows than prompt-only agents.

Get Ready-to-Use Dashboard Templates in Fine Gallery

For executives, the value is concrete: Dora is not an AI experiment. It is a landed AI digital employee for recurring reporting work such as quarterly reporting summaries, close-status briefings, finance risk reporting, disclosure exception alerts, and owner follow-up.

For IT and data teams, the role shifts from manually servicing every reporting request to improving data connections, semantic layers, permission governance, report templates, data quality, and reusable agent Skills.

For business and finance users, the benefit is timeliness and lower friction: they get scheduled summaries, chat-based answers, and exception pushes without searching through multiple files or waiting for analysts to assemble updates.

The strongest Dora pitch is scenario + product + service: FineReport provides the trusted reporting foundation, Dora provides the AI digital employee, and implementation service connects data, governance, semantic setup, Skills, report templates, permissions, and rollout.

SEC rules govern filing obligations, form requirements, and certain disclosure expectations for entities under US securities regulation. GAAP and IFRS are accounting frameworks that determine how transactions are recognized, measured, presented, and disclosed.

No. A company may apply GAAP correctly and still miss SEC-specific requirements related to forms, timing, comparative periods, XBRL, or disclosure content.

It generally applies when a company has securities registered in the United States or is involved in offerings, periodic issuer reporting, or certain material transactions. The exact filing obligation depends on the entity, event, and applicable form.

No. The SEC Financial Reporting Manual is commonly used as an interpretive aid, but it is non-authoritative and does not override Commission rules or accounting standards.

Internal controls help ensure numbers are supported, reviews are documented, and disclosures are consistent across teams and systems. Strong controls reduce reporting risk even in complex close and consolidation environments.

Product Trial

FineReport

Pixel-perfect reports · Interactive dashboards · Easy data entry · Digital twins